Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

Accounting Equation: Definition, Formula, Calculation & Examples

The Accounting Equation explains how business finances stay balanced by showing that assets equal liabilities plus equity and forms the financial statements. It ensures accuracy, supports decision-making, and reflects true financial position. It helps identify errors in records and in managing cash, debt, and investments.

Table Of Contents

44 7452 122728

44 7452 122728

18-Feb-2026

18-Feb-2026

Author-David Walter

Most people think Accounting is about calculations and formulas. In reality, it is about understanding a simple relationship between what a business owns and what it owes. This simple idea is called the Accounting Equation, and it is behind every transaction recorded in a business.

Whether you run a small shop, manage a start-up, or are learning Accounting for the first time, this concept helps you clearly see where money comes from and how it is used. In this blog, we will uncover what is the Accounting Equation, its formula, and its real-world uses to understand business finances with confidence.

What is the Accounting Equation?

The Accounting Equation is the fundamental principle that explains how a business records its financial activities. It shows that everything a company owns comes from either borrowing money or the owner’s investment. Thus, it explains the relationship between a company’s assets, liabilities, and the owner’s equity. The equation is:

Assets = Liabilities + Equity

This Accounting Equation acts as a foundation for financial statements and Double-entry Bookkeeping systems. It also helps Accountants quickly identify errors when the accounts do not balance.

Why the Accounting Equation is the Foundation of Accounting?

Accounting is not only about recording numbers. It is about maintaining financial truth. The Accounting Equation provides a structure that ensures accuracy and reliability in financial records. Here are the reasons why it is the foundation of Accounting:

1) Prevents Errors: If the totals on both sides do not match, Accountants immediately know a mistake exists. The imbalance works like an alarm system.

2) Ensures Transparency: Investors and lenders rely on financial statements. The equation ensures that reported resources are properly funded.

3) Supports Double-entry Bookkeeping: Each transaction has two effects. For example, buying equipment with cash increases equipment but reduces cash.

4) Creates Financial Statements: The balance sheet is actually a presentation of the Accounting Equation in a structured format.

5) Helps Decision-making: Managers can understand how much of the business is financed by debt and how much by owners.

Components of the Accounting Equation

The Accounting Equation is made up of three components: assets, liabilities, and equity. Each represents a different aspect of a business’s financial position. Let's check each of them in detail:

1) Asset in the Accounting Equation

Assets are resources owned or controlled by a business that provides future economic benefits. In simple terms, assets help a company operate and earn revenue. Assets are usually classified into two categories such as current assets and non-current assets.

Current assets are the short-term resources that are expected to be used, sold, or converted into cash within one year, such as cash, inventory, accounts receivable, prepaid expenses, and more. On the other hand, non-current assets are long-term resources used in business operations for more than one year, such as machinery, equipment, vehicles, and buildings.

2) Liability in the Accounting Equation

Liabilities are financial obligations or debts that a business must repay to external parties. They arise when a business borrows money or purchases goods on credit. In simple terms, Liabilities represent other people’s claims on the business’s assets.

Examples of liabilities include supplier payments, bank loans, salaries, taxes, utility bills, mortgages, accounts payable, and more. Managing liabilities properly helps a business maintain good cash flow and financial stability.

3) Shareholders' Equity in the Accounting Equation

Equity represents the owner’s claim on the business after paying all debts. It is sometimes called net worth or capital. It helps understand how much of the business truly belongs to the owner or shareholders.

It usually includes the owner’s investment, retained earnings (profits kept in the business), and any additional capital introduced later. However, it decreases when the business incurs losses or when the owner withdraws money or dividends.

Explore the basics of recording transactions and preparing accounts with Financial Accounting (FFA) Training – Register today!

Impact of Journal Entries on the Accounting Equation

Every business transaction is first recorded as a journal entry, and each entry directly affects the Accounting Equation. Understanding this impact helps explain how daily transactions shape the financial position of a business.

1) Sole Trader

In a sole trader business, the owner and the business are closely connected in Accounting terms. There is only one owner, so the equity part of the equation directly represents the owner’s investment in the business. The Accounting Equation formula will be:

Assets = Liabilities + Owner’s Equity

Example: If the owner invests £1,00,000, both cash (assets) and owner’s equity increase equally. If £10,000 is withdrawn for personal use, cash and equity both decrease, and the equation still balances.

2) Partnership

A partnership consists of two or more individuals who jointly own and operate a business. The Accounting Equation stays the same, but the equity portion is divided among partners based on their ownership share. So, the equation goes like:

Assets = Liabilities + Partners’ Equity

Example: If two partners invest £80,000 and £70,000, assets increase by £150,000 and equity is recorded for each partner separately. Profits are shared and added to each partner’s equity balance.

3) Limited Company

A limited company is legally separate from its owners, who are called shareholders. Because ownership is divided into shares, the equity section becomes more detailed and structured. Here, the equation follows as:

Assets = Liabilities + Shareholders’ Equity

Example: When a company issues shares worth £500,000, both cash and share capital increase. Profits increase retained earnings and total shareholders’ equity.

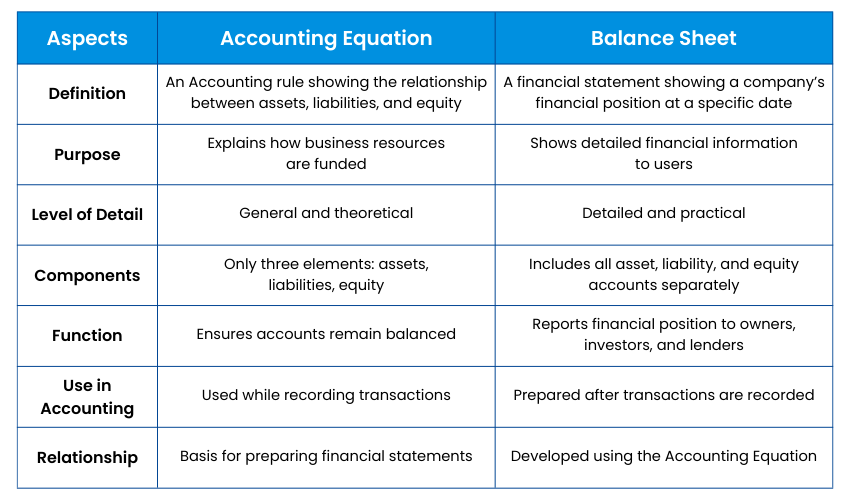

Accounting Equation vs the Balance Sheet

The Accounting Equation and the balance sheet are closely related, but they are not the same thing. The Accounting Equation is a basic rule that shows the relationship between assets, liabilities, and equity. The balance sheet is the financial statement that presents this relationship in a detailed and organised format.

In simple terms, the Accounting Equation is the principle, while the balance sheet is its practical presentation. The balance sheet shows how the accounts balance in a company’s financial report. Below is a detailed difference between the Accounting Equation and the balance sheet:

Examples of Accounting Equation in Real-world

To understand the Accounting Equation better, let us look at an imaginary business and see how real transactions are recorded while keeping the equation balanced. So, let’s assume that a person is starting a small bakery and below are the processes involved:

Step 1: Owner Invests Money

The owner starts the business by investing £200,000 in cash.

Effect:

1) Cash (Asset) increases £200,000

2) Owner’s Capital (Equity) increases by £200,000

Accounting Equation:

Assets (£200,000) = Liabilities (£0) + Equity (£200,000)

The business now has funds to begin operations, and the equation balances.

Step 2: Purchase Equipment

The business purchases ovens and baking equipment worth £80,000 cash.

Effect:

1) Equipment (Asset) increases by £80,000

2) Cash (Asset) decreases by £80,000

Only the form of the asset changes. Total assets remain £200,000.

Accounting Equation:

Assets (£200,000) = Liabilities (£0) + Equity (£200,000)

Step 3: Buy Supplies on Credit

The business buys ingredients worth £30,000 on credit from a supplier.

Effect:

1) Inventory (Asset) increases by £30,000

2) Accounts Payable (Liability) increases by £30,000

Accounting Equation:

Assets (£230,000) = Liabilities (£30,000) + Equity (£200,000)

Step 4: Sales Made to Customers

The business sells its products and receives £50,000 cash.

Effect:

1) Cash (Asset) increases by £50,000

2) Profit increases owner’s equity by £50,000

Accounting Equation:

Assets (£280,000) = Liabilities (£30,000) + Equity (£250,000)

Profit increases the owner’s share in the business.

Step 5: Pay Supplier

The business pays £20,000 to the supplier.

Effect:

1) Cash (Asset) decreases by £20,000

2) Accounts Payable (Liability) decreases by £20,000

Accounting Equation:

Assets (£260,000) = Liabilities (£10,000) + Equity (£250,000)

Step 6: Owner Withdrawal

The owner withdraws £10,000 for personal use.

Effect:

1) Cash (Asset) decreases by £10,000

2) Equity decreases £10,000 ( Drawings )

Accounting Equation:

Assets (£250,000) = Liabilities (£10,000) + Equity (£240,000)

This example shows that every real-life transaction changes at least two elements of the Accounting Equation. However, after each activity, the equation always remains balanced, which proves the accuracy of accounting records.

Learn how businesses control expenses and improve profitability with Managing Costs and Finance (MA2) Training - Sign up soon!

Real-world Applications of the Accounting Equation

Businesses use the Accounting Equation daily to manage finances, track performance, and plan future activities. Let’s look at how it is applied in real-world contexts:

1) Budgeting

When businesses prepare a budget, they rely on the Accounting Equation to understand how much they can spend. For example, if a business wants to buy new equipment, it must decide whether to use its own cash or borrow money. This helps avoid overspending and manage money safely.

2) Financial Analysis

Financial Analysis involves evaluating whether a business is financially healthy. The Accounting Equation helps owners and accountants determine if the company relies too heavily on borrowed funds. It also supports managers in identifying and correcting financial problems when they arise.

3) Investment Decisions

Investors and lenders study financial records before giving money to a business. They check how much the company owns and how much it owes. The Accounting Equation helps them understand how risky the business is. A business with steady profits and reasonable debts looks safer to invest in.

Conclusion

The Accounting Equation may look simple, but it is the core idea behind the entire Accounting system. It connects every transaction, ledger, and financial statement into one logical system. It helps in tracking performance, controlling spending, and making informed decisions. It is a practical tool that helps businesses understand their financial position and operate responsibly.

Build confidence in financial concepts and Bookkeeping with ACCA Foundations Training – Begin now!

Frequently Asked Questions

Q. What is Extended Accounting Equation?

The extended Accounting Equation expands equity into detailed components:

Assets = Liabilities + Capital + Revenue − Expenses − Drawings

It shows how profits, expenses, and withdrawals affect the owner’s equity.

Businesses use it to evaluate performance across accounting periods, rather than only viewing the current financial position.

Q. What is the Most Popular Accounting Equation?

The most popular Accounting Equation is the Basic Accounting Equation:

Assets = Liabilities + Equity

It forms the foundation of Double‑entry Bookkeeping, ensuring every transaction keeps financial records balanced and accurate in any business.

Q. What are the Five Basic Accounting Principles?

The five Accounting principles guide how transactions are recorded and ensure financial statements are reliable. Those include:

1) Revenue recognition principle

2) Matching principle

3) Historical cost principle

4) Full disclosure principle

5) Objectivity principle