Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

What is a Suspense Account? Characteristics and How to Use it

A Suspense Account temporarily records unclear or unidentified transactions until they are examined, resolved, and transferred to the appropriate account. It helps businesses keep their books balanced while they investigate and correct errors. Once verified, Accountants move the amounts to the correct account.

Table Of Contents

44 7452 122728

44 7452 122728

19-Feb-2026

19-Feb-2026

Author-Maria Thompson

Have you ever checked your accounts and found that the numbers do not match, but you cannot see why? Missing details, unclear entries, or small calculation errors can create confusion in financial records. This is why the Suspense Account becomes useful since it acts as a temporary holding place that keeps your books balanced while you track the correct information.

It lets you record the amount safely and fix it later once the facts are clear. It is a practical tool used by businesses and accountants to manage uncertainty without losing control of their records. In this blog, you will explore What is a Suspense Account, its characteristics, importance, how to use one, and more.

What is a Suspense Account?

A Suspense Account is a temporary holding account used in accounting for transactions that cannot be immediately classified. It acts as a placeholder that allows accountants to record an entry right away. This keeps the books balanced and updated while the correct amount is identified, and the entry is later moved to the proper place in the general lodger.

Suspense Account can be imagined as a “mystery box” for uncertain transactions. When a payment, receipt, or journal entry appears, but its purpose is unknown, it is parked here instead of being wrongly recorded. Once the required information is found, the amount is cleared from the account and posted to the correct account.

Characteristics of a Suspense Account

A Suspense Account has certain characteristics that make it different from regular accounts. Let's look at them below:

1) It is a Temporary Account

: A Suspense Account is used for a short period when transaction details are missing or unclear. Once the correct information is available, the entry is transferred to the proper account, and the suspense balance is cleared.

2) It is Part of the General Lodger: A Suspense Account comes within the general lodger. This means every unclear entry is formally recorded to maintain complete and traceable financial records.

3) It Helps in Managing Uncertainty: A Suspense Account enables accountants to record transactions even when details are missing. This reduces delays and prevents forced classifications.

4) It Supports Balanced Books: When totals do not match, or a side of the entry is unknown, the difference can be placed in a Suspense Account. This keeps the trial balance and books aligned.

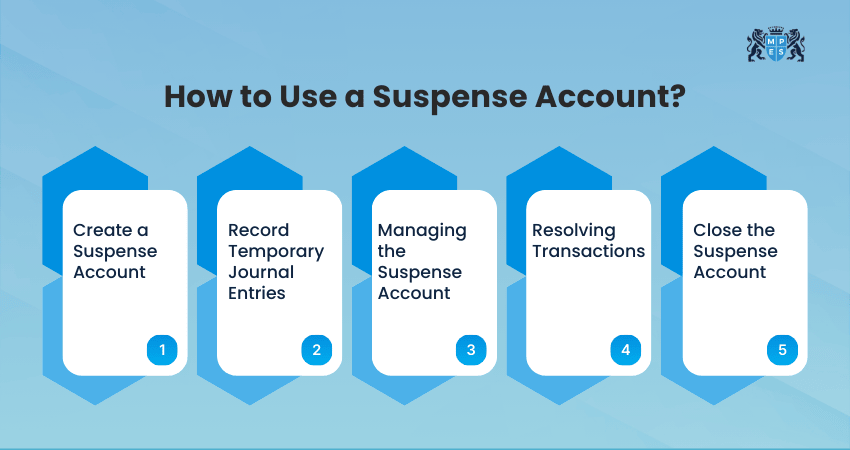

How to Use Suspense Accounts?

Understanding how to use a Suspense Account keeps accounting records accurate and compliant. Let’s look at the practical ways to utilise it below:

1) Create a Suspense Account

When you identify a transaction that cannot be classified, create a Suspense Account in the general ledger. This account works as a temporary holding place for entries that require further checking, supporting documents, or proper classification.

2) Record Temporary Journal Entries

Record the transaction amount in the Suspense Account as a debit or credit. Also, pass the opposite entry in the related account to keep the double-entry system balanced. This ensures your books stay aligned even when the transaction is under review.

3) Managing the Suspense Account

Keep the Suspense Account active only for the period you need it. Review it regularly to identify pending items and investigate their details. One effective practice is clearing each suspense entry quickly and aiming to resolve most items within 30 days to avoid a backlog.

4) Resolving Transactions

Once the correct information is available, remove the amount from the Suspense Account. Then record the transaction in the correct permanent account. This helps to reallocate the amount properly and clears the temporary record.

5) Close the Suspense Account

After all entries are identified and transferred to their correct accounts, close the Suspense Account. This prevents carry-forward errors and ensures your financial statements reflect only properly classified transactions.

Learn modern finance and business strategy with

CIMA’s CGMA® Managing Finance in a Digital World (E1) Course

now!

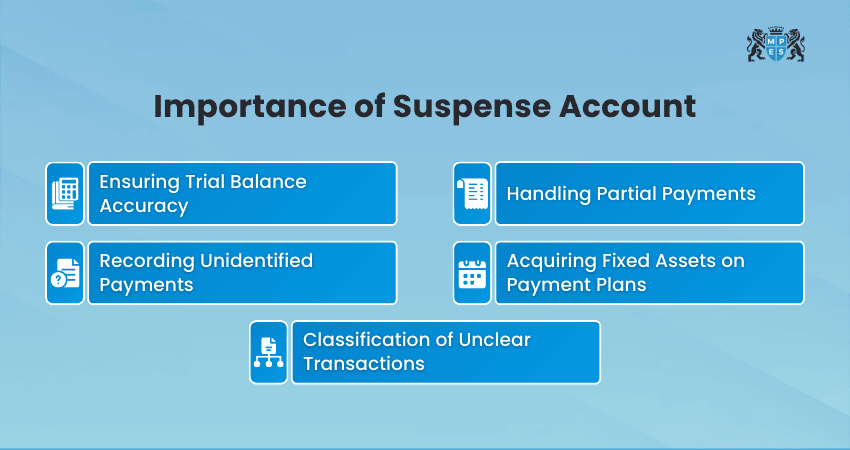

Importance of Suspense Account

A Suspense Account is used to manage transactions that cannot be immediately classified. Let's look at some of the importances of this account below:

1) Ensuring Trial Balance Accuracy

At the end of an accounting period, the total debits and credits may not always match due to posting errors. The difference is temporarily placed in a Suspense Account to keep the trial balance aligned. The account remains open until the error is identified and resolved.

2) Handling Partial Payments

Sometimes, customers make partial payments without clearly stating which invoice they are related to. In this case, the received amount is recorded in a Suspense Account until confirmation is verified. Then the amount is transferred to the correct account.

3) Recording Unidentified Payments

You may receive money in your bank account without clear details of the payer. This can be recorded in the Suspense Account. Meanwhile, match it with open invoices or contact the customer’s bank. After identification, move the entry to the correct account.

4) Acquiring Fixed Assets on Payment Plans

If a fixed asset is being purchased through instalments and ownership is transferred only after full payment, the instalment amount can be posted in the Suspense Account. When the final payment is made and the asset is received, the total is moved to the fixed asset amount.

5) Classification of Unclear Transactions

Small businesses often encounter transactions that are difficult to classify. These can be recorded in a Suspense Account until an accountant reviews them. This keeps records organised and reduces the risk of classification errors.

When to Use Suspense Accounts?

Let’s look at some of the common situations when a Suspense Account must be used below:

1) You’ve Received a Partial Payment

If a customer sends a partial payment and you are not sure which invoice it relates to, place the amount in a Suspense Account. After confirming with the customer, transfer the amount to the correct invoice amount and clear the suspense entry.

2) You’re Preparing a Trial Balance

At the end of an accounting period, you prepare a trial balance to check whether debits and credits match. If they do not match, record the difference in the Suspense Account until the error is found and resolved.

3) You Don’t Know Who a Payment is From

Sometimes a payment is received without clear details of the payer. In such cases, hold the amount in a Suspense Account while you compare it with outstanding invoices and verify the sender. Once confirmed, move the entry to the correct customer account.

4) You Don’t Know How to Classify a Transaction

If you are unsure about which account a transaction belongs to, it is safer to use a Suspense Account. Keep the entry there temporarily and consult your accountant. Once clarified, re-classify it correctly and clear the suspense balance.

5) You Buy a Fixed Asset but Don’t Receive it Until it’s Paid Off

If you are paying for a fixed asset through instalments and ownership is transferred only after full payment, record the instalments in the Suspense Account. After the final payment and delivery, transfer the full amount to the fixed asset account.

Turn numbers into clear financial stories with

CIMA’s CGMA® Financial Reporting Training (F1)

today!

Suspense Account Examples

A Suspense Account is understood through practical scenarios. Let’s look at some practical examples below:

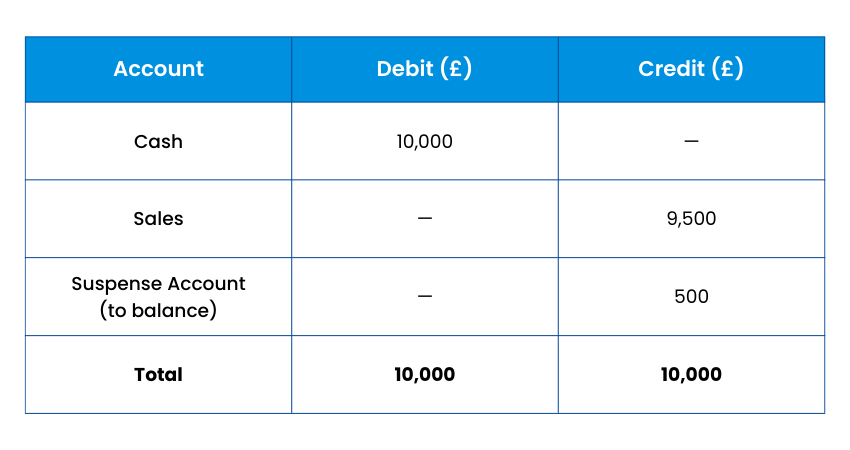

Example 1: Trial Balance Adjustment

When a trial balance does not match, and the error source is unknown, the difference is temporarily placed in the Suspense Account. This keeps the books balanced while the issue is being investigated.

Scenario:

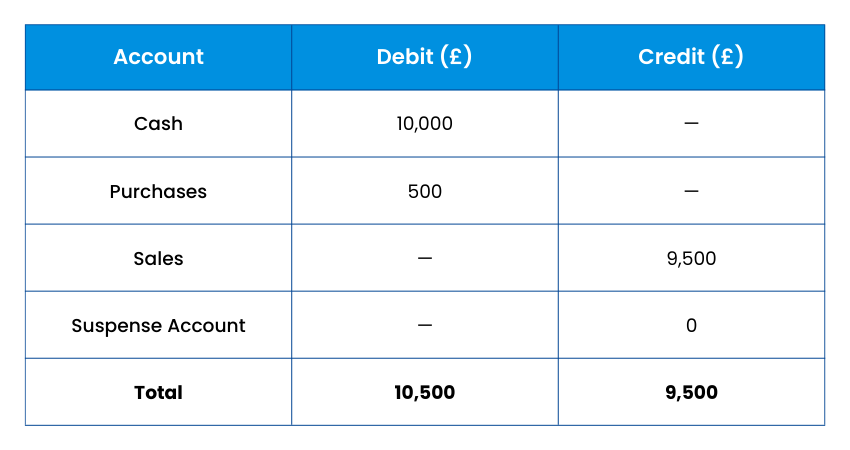

At a company, a £500 difference is found between total debits and credits. A Suspense Account is used until the error is located.

Journal Entries:

Step 1: Initial Entry to Balance the Trial Balance

Step 2: After Error is Identified

Example 2: Unidentified Bank Deposit

When a bank deposit is received but its source or purpose is unknown, it is temporarily held in the Suspense Account until it is verified.

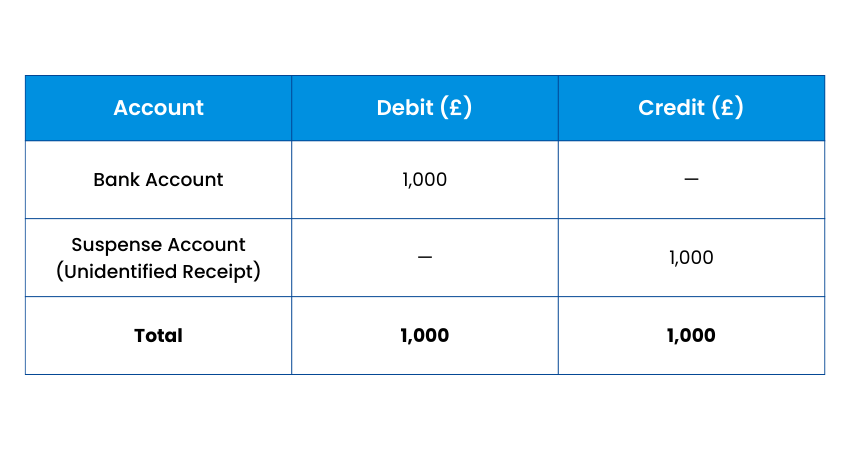

Scenario:

XYZ Ltd. receives a £1,000 deposit with no payment reference. The amount is placed in a Suspense Account while the team is performing an investigation.

Journal Entries:

Step 1: Initial Entry for Unknown Deposit

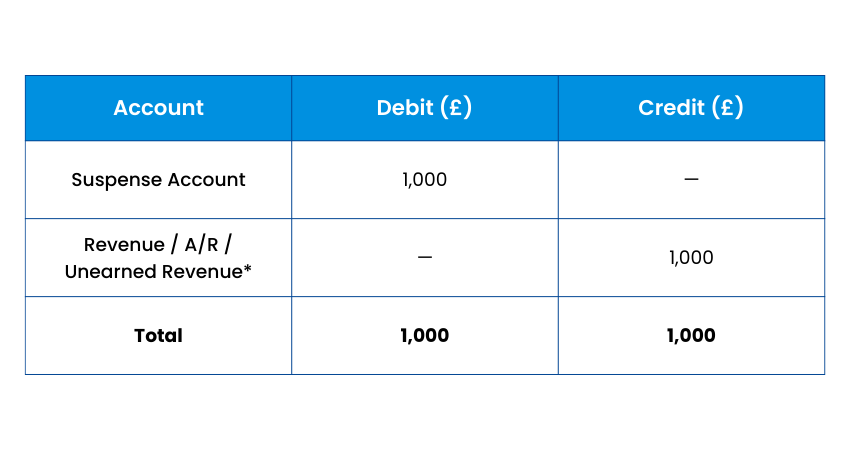

Step 2: After Identification of Deposit Purpose

Practice, apply, and pass the CIMA operational ease study exam with confidence by joining CIMA’s CGMA® Operational Level Case Study Course – Register now!

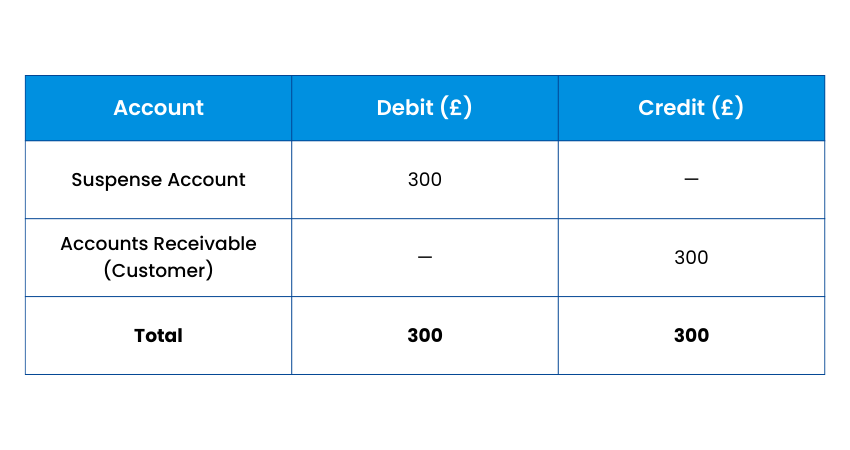

Example 3: Partial Payment on Invoice

When a customer sends a partial payment without invoice details, the amount is parked in a Suspense Account until clarification is received.

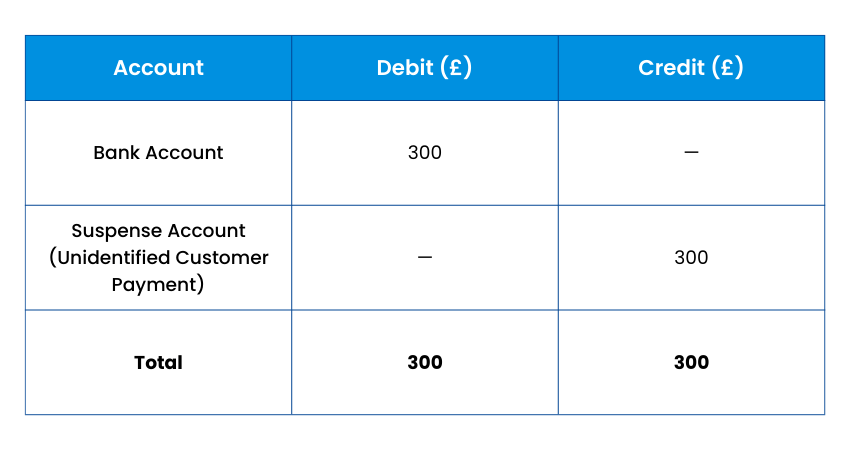

Scenario:

JKL Enterprises receives a £300 payment against a £1,000 invoice, but the invoice number is not mentioned.

Journal Entries:

Step 1: Initial Entry for Partial Payment

Step 2: After Confirming the Correct Invoice

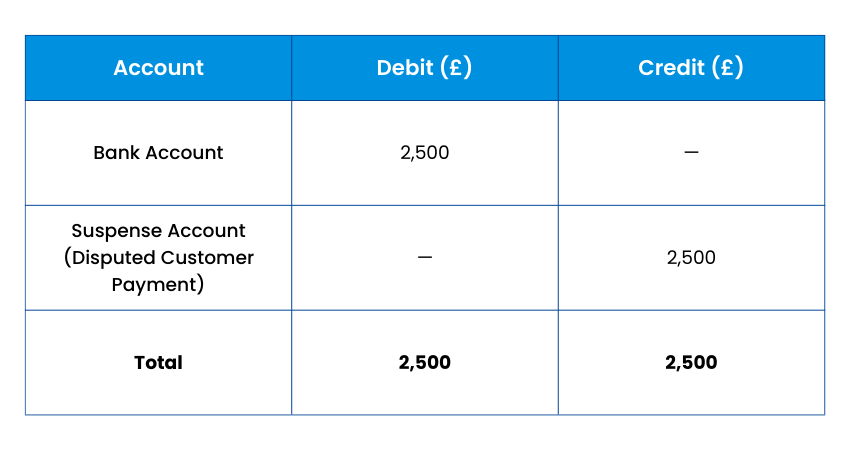

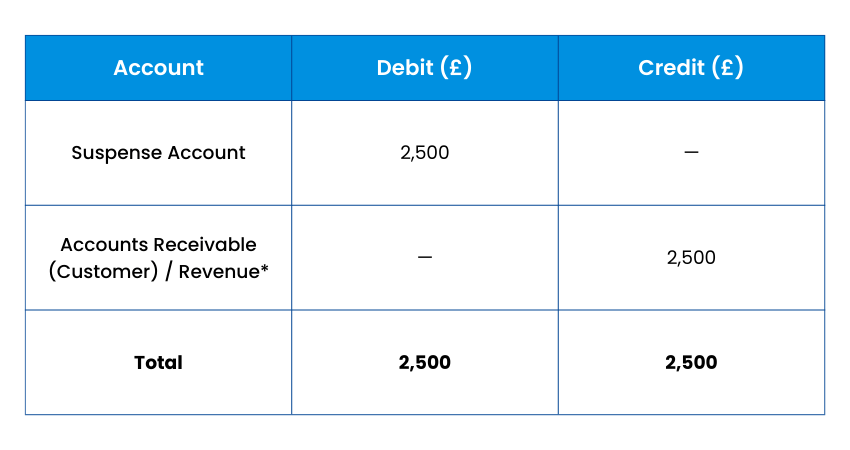

Example 4: Payment With Disputed Charges

When a payment relates to an invoice that includes disputed charges, it is held in the Suspense Account until it is resolved.

Scenario:

MNO Inc. receives a £2,500 from a customer, but the billing items are under dispute. The amount is not immediately recognised as revenue.

Journal Entries:

Step 1: Initial Entry for Disputed Payment

Step 2: After Dispute Resolution

Conclusion

A Suspense Account is a powerful safety net for your accounting records. It helps you to keep your books balanced, organised, and accurate even when transactions are unclear, incomplete, or under review. Using this account correctly helps businesses to avoid misclassifications, reduce errors, and maintain trust in their financial reports.

Build real-world finance skills with CIMA’s CGMA® Operational Level Courses now!

Frequently Asked Questions

Q. How Long Can Funds Stay in Suspense Account?

Funds in a Suspense Account can stay temporarily until the transaction is identified and moved to the correct account. Best practice is to clear it within 5-40 days. Although there is no legal limit, long balances can indicate weak controls.

Q. Is Suspense a Debit or Credit?

A Suspense Account can have either a debit or a credit balance because it temporarily holds unclassified entries. It is used to balance the trial balance until the error is found and cleared.

Q. Is a Suspense Account a Liability or Asset?

A Suspense Account can be either a liability or an asset, depending on the type of transaction it is temporarily holding. If it has a debit balance, it is treated as an asset, or if it has a credit balance, it is treated like a liability until cleared.