Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

What are Assets in Accounting: A Comprehensive Guide

Assets in Accounting are resources a business owns or controls that provide future economic benefits, including items such as cash, inventory, machinery, etc. They are classified into current and fixed, tangible and intangible, and operating and non-operating assets. They help businesses operate efficiently and generate revenue over time.

Table Of Contents

44 7452 122728

44 7452 122728

12-Feb-2026

12-Feb-2026

Author-Maria Thompson

Every successful business, whether small or international, is built on one powerful foundation: its assets. From the cash it holds to the equipment it uses and the brand reputation it builds over time, these resources quietly drive performance and growth. But what are Assets exactly?

Do they include cash and physical items like buildings and machinery, or do they also cover elements like software and goodwill? How are they measured, and why are they so important in accounting? In this blog, we will discover What are Assets in Accounting, their types, and how they appear in financial statements. Let's dive in!

What are Assets in Accounting?

In accounting terms, Assets are any resources owned or controlled by a business that are expected to provide financial benefits in the future. They are generally listed on the balance sheet and represent what a business owns. They can include cash, company vehicles, equipment, inventory, and other valuable resources.

In simple terms, Assets in Accounting are the things that a business can use, sell, or rent to generate revenue, either in the present or in the future. They play an important role in supporting daily business operations and long-term growth.

The Importance of Assets in Accounting

Assets are not just items a business owns; they are the foundation of financial strength and operational success. Understanding their importance helps businesses manage resources wisely and maintain long-term stability. Let's check them:

1) Measure Financial Strength: Assets help show how strong a company is. If a business owns valuable resources, it usually means it is stable and able to handle financial challenges.

2) Support Daily Operations: Many assets, such as cash, inventory, and equipment, are used every day. Without these, a business cannot operate properly or serve its customers.

3) Improve Liquidity and Cash Flow: Current assets like cash and money from customers help a business pay short-term expenses and debts. This keeps the company financially safe and organised.

4) Attract Investors and Lenders: Investors and banks look at a company’s assets before giving money. Strong assets make the business look more reliable and trustworthy.

5) Help in Strategic Planning: Knowing the asset information helps managers plan for the future. It supports decisions about growth, new investments, and cost control.

6) Determine Business Value: The total value of assets helps determine how much the business is worth.

7) Enhance Financial Reporting: Recording assets correctly makes financial statements accurate and clear, which helps to understand the company’s real position.

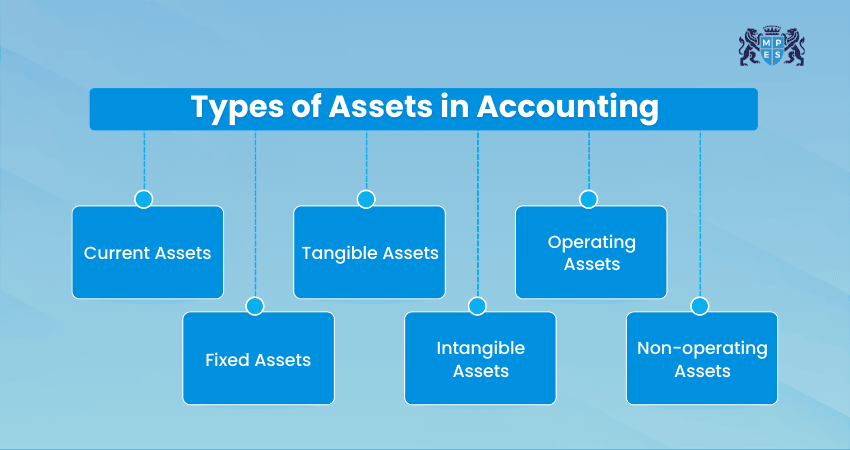

Types of Assets in Accounting

Assets in Accounting are classified in different ways to provide clarity and structure in financial reporting. Let us explore the major categories:

1) Current Assets

Current assets are short-term resources that are expected to be used, sold, or converted into cash within one accounting year. While some current assets are highly liquid, not all can be immediately converted into cash. Common examples include:

1) Cash and cash equivalents

2) Accounts receivable

3) Inventory

4) Short-term investments

5) Prepaid expenses

2) Fixed Assets

Fixed assets, also known as non-current assets or long-term assets, are resources that a business intends to use for more than one year. Examples of this type of asset are:

1) Buildings

2) Machinery

3) Vehicles

4) Equipment

5) Land

3) Tangible Assets

Tangible assets are physical resources that can be seen and touched. They include both current and fixed assets with a measurable physical presence. These assets are usually easier to measure because they have a clear purchase price and physical presence. Examples include:

1) Equipment

2) Inventory

3) Property

4) Vehicles

4) Intangible Assets

Intangible assets do not have a physical form. You cannot touch them, but they still have value. They are the long-term resources that provide a great advantage to a business. Key examples of this type involve:

1) Patents and copyrights

2) Trademarks

3) Brand names

4) Goodwill

5) Software and databases

5) Operating Assets

Operating assets are directly used in the daily operations of a business. They involve both tangible and intangible assets that can generate revenue. They are essential for a business to function properly. Examples are:

1) Cash

2) Inventory

3) Equipment

4) Accounts receivable

5) Raw materials

6) Non-operating Assets

Non-operating assets are not essential to daily operations but still provide value to your organisation. These may generate additional income or be sold in the future, but they are not critical to core business activities. Key examples include:

1) Marketable securities

2) Unused land

3) Spare equipment

4) Excess cash

5) Investment property

Prepare for the future of finance with

CIMA’s CGMA® Managing Finance in a Digital World (E1) Course

– Register today!

How are Assets Valued in Accounting?

Valuing Assets in Accounting means deciding how much they are worth in financial records. It is one of the most important aspects of accounting. Different methods are used depending on the asset type and accounting standards. Those methods include the following:

1) Historical Cost

The historical cost records an asset at the price paid when it was purchased. This includes all costs needed to make the asset ready to use. For example, if a machine costs £40,000 and installation costs £3,000, the total recorded value is £43,000. This method is reliable because it is based on actual transactions. However, it does not show the current market value.

2) Fair Market Value

Fair Market Value (FMV) is the price an asset would sell for today in an open market. It reflects current demand and supply in the market rather than the original purchase price. It may provide a more realistic picture of asset value, but it can fluctuate based on market conditions. This method is often used for investments or properties.

3) Depreciation

Depreciation does not determine the original value of an asset but allocates its cost over its useful life. Instead of recording the full cost as an expense in one year, the business divides the cost across several years. For example, if equipment costs £10,000 and lasts five years, £2,000 may be recorded as an annual expense. This ensures expenses match the income generated by the asset.

4) Impairment

Impairment happens when an asset loses value unexpectedly. If an asset loses value due to damage, obsolescence, or market decline, an impairment loss is recorded. For example, technological advancements may reduce the usefulness of certain equipment. In such cases, accounting standards require the asset value to be adjusted downward.

How Assets Appear on the Balance Sheet?

In general, assets appear at the top of the balance sheet and are listed in the order of liquidity. Liquidity means how fast an asset can be turned into cash. Therefore, current assets appear first because they can be converted into cash quickly. They are followed by non-current assets.

The balance sheet follows this basic formula:

Assets = Liabilities + Equity

Liabilities are the amounts a business owes to others, and equity represents the owners’ share in the business. The total assets figure helps people understand the size and strength of the business.

Enhance your financial statements and reporting standards with

CIMA’s CGMA® Financial Reporting Training (F1)

- Sign up soon!

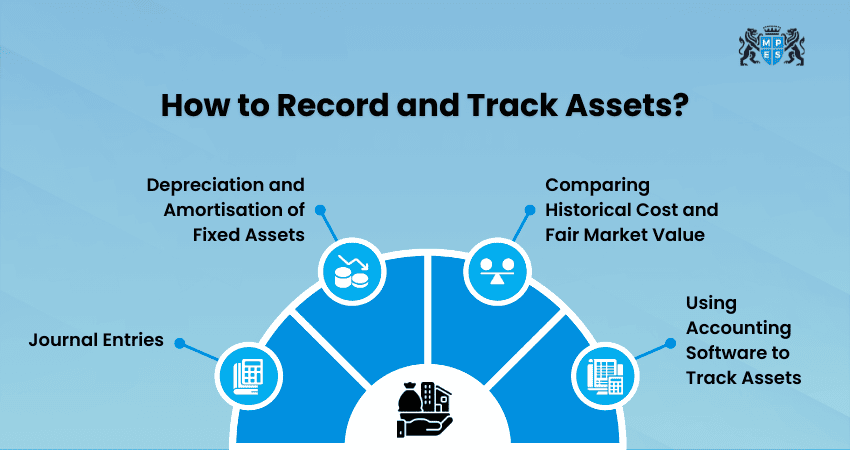

How Assets are Recorded and Tracked in Accounting?

Recording and tracking assets in the right way is important for maintaining accurate financial records. Let's check the ways you can record and track them:

1) Journal Entries

Whenever a business buys or sells an asset, it is recorded in a journal using double-entry accounting, where one account is debited, and another is credited to keep the books balanced. In simple terms, if one account increases, another has to decrease, or a liability must increase.

For example, if a business purchases machinery worth £10,000 by taking a bank loan, the entry would be:

1) Debit: Machinery £10,000

2) Credit: Bank loan (liability) £10,000

2) Depreciation and Amortisation of Fixed Assets

Amortisation is the process of gradually spreading the cost of an intangible asset, such as software or a patent, over its useful life. So, depreciation applies to tangible assets, while amortisation applies to intangible assets.

For example, software costing £10,000 with a five-year life may be amortised at £2,000 per year.

3) Comparing Historical Cost and Fair Market Value

Historical cost records an asset at its original purchase price, while fair market value reflects the price the asset could sell for under current market conditions. Historical cost is more stable and verifiable, whereas fair market value provides a more current view of asset worth.

For example, if land was purchased for £50,000, it is recorded at that amount under historical cost. If its current market value rises to £80,000, the fair market value would reflect £80,000, subject to applicable accounting standards.

4) Using Accounting Software to Track Assets

Nowadays, many businesses use Accounting Software to track assets. This software records purchase details, calculates depreciation automatically, and keeps asset registers updated.

Popular examples of Accounting Software include QuickBooks, Xero, Sage, Zoho Books, and FreshBooks. They help reduce human errors and make Financial Management easier.

Common Mistakes Businesses Make When Recording Assets

Even small mistakes in Asset Accounting can cause problems. Some of the most common mistakes that businesses make while recording assets include:

1) Treating Expenses as Assets: Incorrectly capitalising regular expenses—such as routine repairs or maintenance—can overstate asset values and misrepresent financial statements.

2) Forgetting Depreciation: Not recording depreciation accurately over an asset’s useful life causes assets to appear more valuable than they actually are and reduces expense accuracy.

3) Ignoring Asset Impairment: Failing to adjust asset values when they decline due to damage, obsolescence, or market conditions can present a misleading view of the company’s financial health.

4) Poor Asset Record Management: Missing important details such as purchase date, acquisition cost, useful life, or asset location can lead to errors during audits and financial reviews.

5) Overvaluing Intangible Assets: Assigning excessive value to items like goodwill, trademarks, or brand reputation can distort the company’s true net worth, especially when recognition criteria are not met.

6) Incomplete Supporting Documentation:

Not retaining invoices, contracts, or receipts may cause issues during tax assessments, compliance checks, audits, or valuation reviews.

Examples of Assets in Different Businesses

Assets can look very different depending on the type of business. Exploring how they vary across industries helps you see how businesses operate and where their true value lies. Below are some of the examples:

1) SaaS Company

A Software as a Service (SaaS) company mainly relies on digital and intangible assets. Physical assets may be limited to office equipment. Most value lies in technology and brand reputation. Examples of assets include:

1) Proprietary software platforms

2) Intellectual property such as source code and patents

3) Customer contracts and subscription agreements

4) Brand value and goodwill

2) Retail Business

A retail business depends heavily on tangible and operating assets. Inventory is especially important in this because it directly affects sales and profit. Assets can be in the form of:

1) Inventory and stock

2) Shelving and display equipment

3) Delivery vehicles

4) Warehouse storage facilities

3) Service-based Business

Service-based companies often have fewer physical assets because they mainly offer skills, expertise, or professional services. However, they still have important assets. Those include:

1) Office equipment

2) Professional licences

3) Client databases

4) Company vehicles

Conclusion

Assets form the foundation of every business. Whether it is cash for daily expenses, equipment used in production, or inventory ready for sale, each asset plays an important role in building financial strength. With a strong knowledge of What are Assets in Accounting, Business Owners can make better decisions, manage risks, and plan for long-term financial stability with confidence.

Gain practical skills to succeed in Management Accounting with CIMA’s CGMA® Operational Level Training – Begin today!

Frequently Asked Questions

Q. What are the Seven Current Assets?

There is no fixed rule that limits current assets to exactly seven categories, but the following are commonly recognised examples of current assets:

1) Cash

2) Cash equivalents

3) Accounts receivable

4) Inventory

5) Prepaid expenses

6) Marketable securities

7) Short-term investments

Q. What are Assets and Liabilities?

Assets are resources owned or controlled by a business that are expected to provide future economic benefits. Liabilities are financial obligations the business owes to others, such as loans, unpaid bills, or outstanding expenses.

Q. Is Cash an Asset?

Yes, cash is a primary current asset because it is the most liquid resource a business holds, as it can be used immediately to pay expenses, settle debts, or invest in opportunities.