Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

Payment Reconciliation: Definition, Types, and Benefits Explained

Payment Reconciliation is the process of matching internal financial records with external bank statements to maintain reliable financial reporting. It helps businesses identify errors, prevent fraud, and ensure accuracy. It also aims to streamline operations and ensure all transactions are correctly recorded and accounted for.Table Of Contents

44 7452 122728

44 7452 122728

11-Apr-2026

11-Apr-2026

Author-Maria Thompson

Are you sure every payment in your business records is actually correct? It might look like a simple question, but in reality, even small mismatches in financial records can create bigger problems. A missing entry, duplicate transaction or delayed update can quietly affect your financial accuracy. This is where Payment Reconciliation becomes essential.

It helps businesses avoid costly errors, maintain control over cash flow, and ensure financial confidence. In this blog, we will explore what is Payment Reconciliation, why it matters, the different types involved, and how businesses can use it to maintain reliable financial records. Let's dive in!

What is Payment Reconciliation?

Payment Reconciliation is the process of comparing a company’s internal financial records with external sources, such as bank statements or payment systems, to ensure that all transactions match correctly. It helps businesses confirm that the money they expect to receive or pay has been properly recorded and reflected in their accounts.

In simple terms, it acts as a way to double-check financial data. By reviewing and matching transactions regularly, businesses can identify missing entries, incorrect amounts, or duplicate records.

Importance of Payment Reconciliation

Payment Reconciliation is essential for ensuring that all incoming and outgoing transactions are accurately recorded and matched with financial statements. It helps businesses detect discrepancies, prevent errors, and identify any unauthorised or fraudulent activities. By maintaining accurate records, organisations can ensure financial transparency and compliance with regulations.

Regular reconciliation also improves cash flow management and supports better financial decision making. It allows businesses to track payments, manage outstanding balances, and maintain strong relationships with vendors and customers. Overall, it strengthens financial control and ensures smooth day-to-day operations.

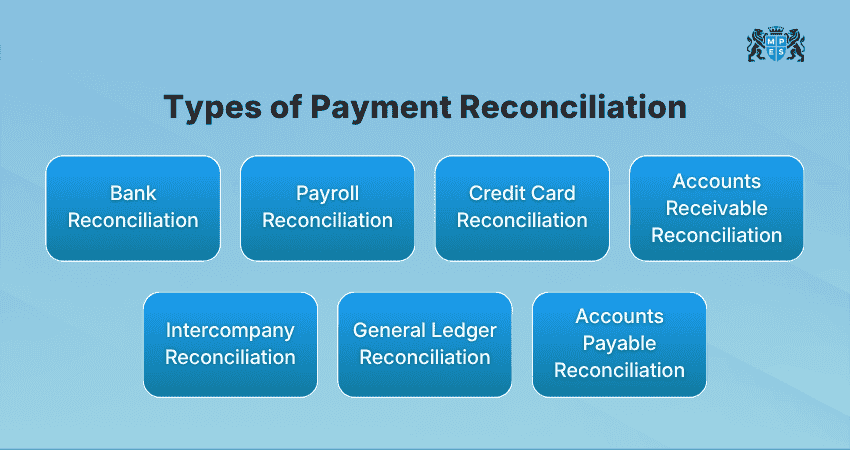

Types of Payment Reconciliation

Different types of Payment Reconciliation have various purposes within an organisation. Each of them focuses on a specific area of financial activity, ensuring that all aspects of transactions are properly verified. Here are the most common types:

1) Bank Reconciliation

Bank reconciliation involves matching the transactions recorded in the company’s cash account with those shown on the bank statement. The goal is to ensure that the balance in the accounting records matches the balance reported by the bank.

This process helps identify differences such as pending transactions, bank charges, or missed entries. Regular Bank Reconciliation ensures that the business has a clear and accurate view of its cash position.

2) Payroll Reconciliation

Payroll reconciliation involves verifying payroll transactions such as wages, deductions, and taxes. It is done by comparing payroll records and deductions with bank statements and supporting documents.

This process ensures that employees are paid correctly and that all payroll-related deductions and taxes are properly accounted for. It also helps maintain compliance with legal and regulatory requirements.

3) Credit Card Reconciliation

Credit card reconciliation is similar to bank reconciliation but focuses specifically on credit card accounts. It involves comparing transactions recorded in the accounting system with those listed on credit card statements.

This helps businesses verify expenses, ensure accuracy, and detect any unauthorised or fraudulent transactions. It is especially useful for organisations that rely on corporate credit cards for daily operations.

4) Accounts Receivable Reconciliation

Accounts receivable reconciliation involves matching customer payments and credit notes against the invoices issued. It ensures that all incoming payments are correctly recorded and linked to the right invoices.

This process helps businesses identify discrepancies such as underpayments, overpayments, or missing payments. It also supports better Cash Flow Analysis and keeps customer accounts accurate.

5) Intercompany Reconciliation

Intercompany reconciliation is used by businesses that have multiple subsidiaries or divisions. It involves matching transactions that occur between different entities within the same organisation.

This process ensures that all intercompany transactions are recorded consistently across each entity’s financial records. It helps avoid mismatches during consolidation and improves the accuracy of group financial statements.

6) General Ledger Reconciliation

General ledger reconciliation is a broader process that involves reviewing and verifying balances in the general ledger. It includes matching ledger accounts with supporting documents or sub-ledgers.

This type of reconciliation ensures that all financial transactions are correctly recorded and classified. It plays a key role in maintaining accurate financial statements and preparing for audits.

7) Accounts Payable Reconciliation

Accounts payable reconciliation focuses on matching supplier invoices, credit notes, and payments with the records in the accounts payable ledger. It ensures that the business is paying the correct amounts to its suppliers.

By doing this regularly, businesses can avoid duplicate payments, missed payments, and disputes with suppliers. It also helps maintain strong supplier relationships and financial discipline.

Develop essential accounting knowledge and skills with the Financial Accounting (FFA) Course – Register today!

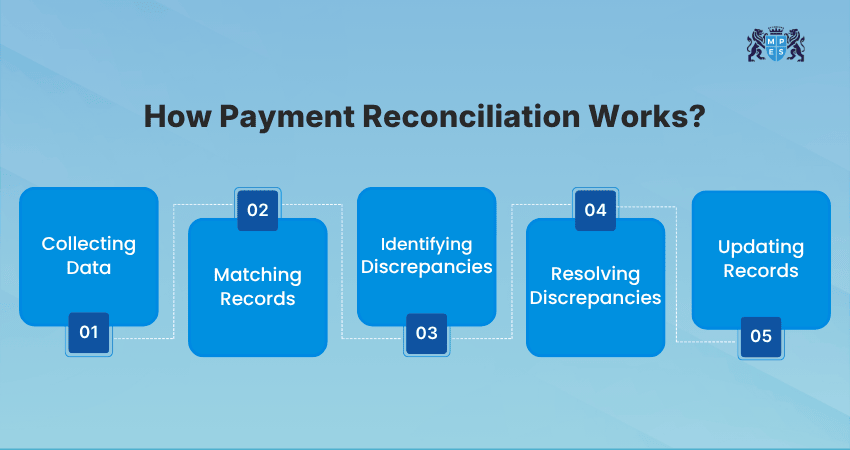

How Payment Reconciliation Works?

Payment Reconciliation follows a structured process to check and verify the financial records. Let's check how it is done:

1) Collecting Data

The first step is gathering all relevant financial data. This includes bank statements, payment gateway reports, invoices, receipts, and internal accounting records.

Key Tips:

1) Use a centralised system to store all financial data

2) Ensure data is collected from all payment channels

3) Schedule data collection at regular intervals

4) Verify the completeness of the data before starting

5) Keep historical records for comparison

2) Matching Records

Once the data is collected, transactions are matched across different sources. For example, a payment recorded in the accounting system is compared with the corresponding entry in the bank statement.

Key Tips:

1) Use unique transaction IDs for easier matching

2) Group transactions by date or reference number

3) Apply automated matching tools where possible

4) Handle bulk transactions using batch processing

5) Flag unmatched entries for further review

3) Identifying Discrepancies

After matching records, any differences between the data sources are identified. These discrepancies could include missing transactions, incorrect amounts, or duplicate entries.

Key Tips:

1) Categorise discrepancies based on type

2) Prioritise high-value discrepancies first

3) Check for timing differences in transactions

4) Review system logs for missing entries

5) Look for duplicate or reversed transactions

4) Resolving Discrepancies

Once discrepancies are identified, the next step is to investigate and resolve them. This may involve correcting errors, updating records, or contacting banks or customers for clarification.

Key Tips:

1) Assign responsibility for issue resolution

2) Maintain clear documentation of actions taken

3) Set timelines for resolving discrepancies

4) Escalate unresolved issues when necessary

5) Track recurring issues to find root causes

5) Updating Records

The final step is updating the financial records to reflect the corrected information. This ensures that all systems are aligned and that the organisation’s financial data is accurate.

Key Tips:

1) Ensure updates are made in all relevant systems

2) Backup data before making major updates

3) Review entries after updates are completed

4) Lock finalised records to prevent changes

5) Conduct a final review before closing the cycle

Understand budgeting, cost control and financial planning with Managing Costs and Finance (MA2) Training – Join now!

Benefits of Automated Payment Reconciliation

As businesses handle increasing volumes of transactions, manual reconciliation can become time-consuming and difficult to manage. Automated Payment Reconciliation offers a more efficient and reliable way to handle this process. Let's explore the key benefits below:

1) Reduced Time and Effort

Automated reconciliation significantly reduces the time and effort required to match transactions. Tasks that once took hours or days can now be completed in minutes. This allows finance teams to focus on more strategic activities rather than repetitive manual work.

It also makes the process smoother by reducing the need for manual data entry and checks. Since the work can be done quickly, businesses can perform reconciliation more often, improving efficiency and keeping financial records updated without delays.

2) Quicker Error Detection

Automation enables real-time or near real-time detection of discrepancies. This means errors can be identified and resolved quickly, reducing the risk of financial inaccuracies. Faster error detection also improves overall financial control and transparency.

In addition, automated systems can flag unusual patterns or inconsistencies instantly, allowing businesses to take immediate action. This proactive approach helps prevent small errors from turning into larger financial issues over time.

3) Enhanced Accuracy and Auditability

Automated systems minimise human errors and ensure consistent processing of transactions. They also provide detailed audit trails, making it easier to track and verify financial data. This is particularly beneficial during audits, as it simplifies the process of demonstrating compliance.

Moreover, having a clear and well-documented record of transactions improves accountability within the organisation. It ensures that every change or update is traceable, which strengthens internal controls.

4) Scalable Operations

As businesses expand, the volume of transactions increases. Automated Payment Reconciliation systems can handle large volumes of data without compromising accuracy or efficiency. This scalability makes automation an essential tool for growing organisations.

It also allows businesses to adapt easily to new payment methods, markets, or systems without needing major changes in processes. This flexibility ensures that financial operations remain smooth and efficient even as the business continues to grow.

Gain the confidence to handle financial tasks effectively with ACCA Foundations Training – Sign up soon!

Challenges of Manual Payment Reconciliation

While manual Payment Reconciliation may work for smaller transaction volumes, it becomes increasingly difficult as businesses grow. It may come with challenges like:

1) Reliance on Manual Processes and Disconnected Systems

Manual reconciliation often involves multiple systems and spreadsheets, making it difficult to maintain consistency. Data may need to be transferred between systems, increasing the risk of errors. Disconnected systems can also lead to delays and inefficiencies in the reconciliation process.

2) Risk of Human Errors and Missing Records

Human errors are a common issue in manual reconciliation. Mistakes such as incorrect data entry or overlooked transactions can result in discrepancies in financial records. Missing records can further complicate the process, making it difficult to achieve accurate reconciliation.

3) Inconsistent or Lack of Standardised Processes

When different teams or individuals follow their own methods for recording and reconciling transactions, it creates confusion and increases the chances of errors. Without standardised processes, the same task may be handled differently each time, leading to mismatched records and unreliable results.

4) Growing Payment Complexity

With the rise of digital payments, businesses now deal with multiple payment methods, currencies, and platforms. Managing these channels at the same time can make it difficult to keep records aligned. This complexity adds pressure on manual systems, making them slower and more prone to errors.

Payment Reconciliation Best Practices

To get the best results from Payment Reconciliation, businesses need to follow a clear and simple approach. Here are the best practices you can follow to reduce errors, improve accuracy, and make the process easier to manage:

1) Leverage Automation Where Possible

Using automated tools can make the reconciliation process faster and more accurate. This is because automation reduces the need for manual work, which lowers the chances of human errors. It also helps businesses handle large volumes of transactions easily and allows real-time tracking, making the entire process reliable.

2) Ensure Regular and Timely Reconciliation

Reconciliation needs to be done regularly, whether daily or monthly, depending on the business needs. Doing it on time helps identify errors early, even before they become bigger problems. Regular checks also keep financial records up to date and make it easier to manage cash flow and reporting without last-minute stress.

3) Maintain Segregation of Duties

Assign responsibilities to different people for various parts of the reconciliation process. For example, one person records transactions while another reviews them. This minimises the risk of fraud and errors, as no single person has full control over the entire process. It also improves accountability within the team.

4) Standardise the Reconciliation Process

Having a clear and consistent process ensures that Payment Reconciliation is carried out in the same way every time. This reduces confusion, avoids mistakes and improves accuracy. It also makes it easier for teams to follow the process, especially when new employees are involved, and ensures consistency across different departments within the organisation.

5) Address Discrepancies Promptly

Any differences found during reconciliation should be resolved as soon as possible. Delaying this can lead to bigger issues and more complicated errors later. Moreover, quick action helps keep financial records accurate and ensures that problems are fixed before they affect business decisions.

6) Ensure Security and Controlled Access

Financial data should be protected by allowing access only to authorised individuals. This helps prevent unauthorised changes, data misuse, or potential security risks. Using secure systems, strong passwords, and proper access controls ensures that sensitive financial information stays safe. It also helps maintain trust and keeps financial records reliable and protected.

Conclusion

Payment Reconciliation is a key process that helps businesses keep their financial records accurate, organised, and reliable. By regularly matching transactions and identifying discrepancies, organisations can avoid errors, prevent fraud, and maintain better control over their finances. In the long run, it not only supports accurate reporting but also builds confidence, improves decision-making, and ensures financial stability.

Looking to build strong accounting fundamentals? Begin your journey with the Maintaining Financial Records (FA2) Course now!

Frequently Asked Questions

Q. What is an Example of a Payment Reconciliation?

An example of Payment Reconciliation is matching a company’s sales records with its bank statement. For instance, if a business records £10,000 in customer payments, it will compare this amount with the bank statement to ensure the same amount has been received and recorded correctly.

Q. What is the Purpose of Payment Reconciliation?

The primary purpose of Payment Reconciliation is to ensure that financial records are accurate and complete. It helps identify errors, prevent fraud, and maintain reliable financial data for reporting and decision-making.

Q. What is the Difference Between Payment Reconciliation and Bank Reconciliation?

Payment Reconciliation covers checking transactions across multiple systems, such as invoices and payment platforms. On the other hand, bank reconciliation focuses only on matching company records with bank statements.