Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

What is an Escrow Account and How Does It Work? Explained

An Escrow Account is a secure financial arrangement where a third party holds money or assets on behalf of two parties until specific conditions are met. It helps reduce risks and ensures a fair and smooth transaction. This builds trust, especially in high-value deals, and is commonly used in business transactions and online payments.Table Of Contents

44 7452 122728

44 7452 122728

28-Apr-2026

28-Apr-2026

Author-James Smith

Imagine this, would you feel comfortable sending a large amount of money to someone you don’t fully trust? For most people, the answer is no and that is when financial transactions begin to feel risky. When large sums are involved, both parties often hesitate, unsure of who should take the first step or how to ensure the deal is fair.

This is where an Escrow Account provides a practical solution. It works as a secure middle ground and adds a layer of security. In this blog, we will explore What is an Escrow Account, how it works, and why it is widely used in secure financial dealings. Let's get started!

What is Escrow?

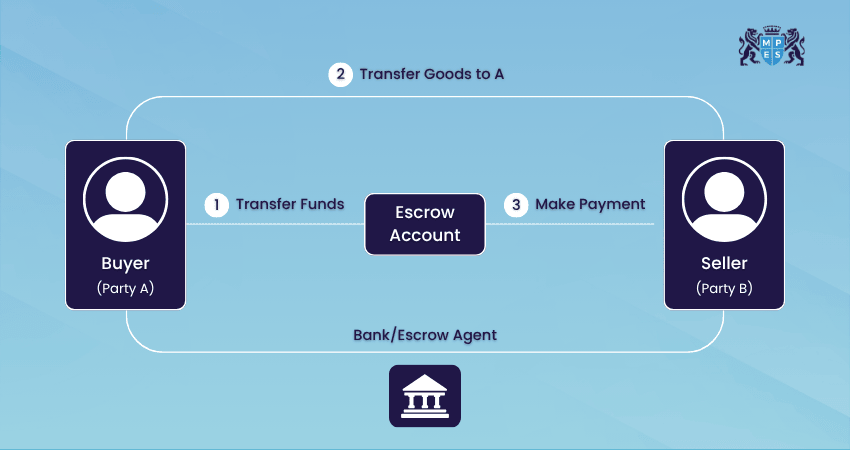

Escrow is a legal and financial arrangement where a neutral third party holds money or assets for two people or businesses involved in a transaction. The funds are only released when all the agreed conditions between both sides are completed.

In this, neither the buyer nor the seller has direct control over the money during the transaction, which ensures fairness and accountability on both sides. Thus, this system is widely used to make transactions safer, reduce misunderstandings, and build trust between parties who may not know each other well.

What is an Escrow Account?

An Escrow Account is a secure account where money or assets are held by a trusted third party (Escrow) during a transaction. The funds stay in this account until all agreed conditions between the parties are fulfilled. Once everything is completed as per the agreement, the funds are released to the appropriate party.

How Escrow Works?

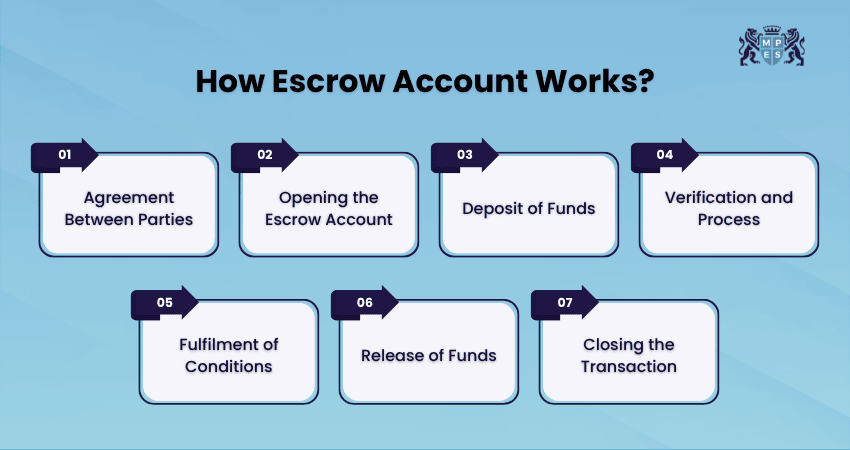

Understanding how Escrow works helps you see why it is such a reliable method for handling financial transactions. Here is the step‑by‑step process:

1) Agreement Between Parties:

Both parties agree on the terms of the transaction, including conditions that must be met before the money is released. These details are clearly written in a contract.

2) Opening the Escrow Account:

A trusted third party, known as an Escrow agent, sets up the Escrow Account to hold the funds securely during the process.

3) Deposit of Funds:

The buyer deposits the agreed amount into the Escrow Account. This shows commitment and ensures the funds are available.

4) Verification and Process:

The Escrow agent holds the money while both parties complete their responsibilities, such as inspections, approvals, or document verification.

5) Fulfilment of Conditions:

All agreed conditions are checked and confirmed. This step ensures that both sides have met their obligations as per the contract.

6) Release of Funds:

Once everything is completed, the Escrow Agent releases the funds to the seller or the appropriate party.

7) Closing the Transaction:

After the funds are disbursed, the Escrow Account is closed, and the transaction is considered complete.

Setting up an Escrow Account

Setting up an Escrow Account is very straightforward, but it involves careful coordination between all parties involved. The first step is selecting a reliable Escrow agent. This could be a bank, legal firm, or licensed Escrow company. Choosing a trustworthy agent is crucial, as they are responsible for managing the funds securely.

Once selected, the terms of the Escrow agreement are defined. These terms outline:

1) How much money will be deposited

2) When will the money be released

3) Conditions for releasing funds

4) Responsibilities of each party

After the agreement is signed, the buyer deposits the funds into the Escrow Account. From there, the Escrow agent manages the account until the transaction is completed.

Why are Escrow Accounts Important for Real Estate Professionals?

For real estate professionals, Escrow Accounts are not just helpful; they are essential. First, they build trust. Buyers feel confident that their money is protected, and sellers know the buyer is serious. Second, Escrow helps follow legal rules. In many places, using an Escrow is required for property deals.

Escrow Accounts also reduce stress for real estate agents. It also simplifies financial management and they don’t have to handle money directly, which lowers the risk of mistakes.

Strengthen your expertise in managing finances with the Financial Management (FM) Course – Register today!

Types of Escrow Accounts

Escrow Accounts are used in different situations, depending on the purpose of the transaction. So, let’s check some of its most common types:

1) Homebuyer's Escrow

A homebuyer’s Escrow Account is used during the property purchase process. It temporarily holds the buyer’s funds until the transaction is complete. This type of Escrow often includes earnest money deposits, which demonstrate the buyer’s commitment to purchasing the property. It ensures that the funds are protected while key steps, such as inspections and legal checks, are completed.

2) Homeowner's Escrow

After purchasing a home, many homeowners continue to use Escrow Accounts as part of their mortgage agreement. In this case, the Escrow Account is used to manage ongoing expenses like property taxes and insurance. The lender collects a portion of these costs along with the monthly mortgage payment and holds it in Escrow. When payments are due, the lender pays them on behalf of the homeowner, ensuring timely and organised financial management.

3) Business Transaction Escrow

A business transaction Escrow Account is used when companies enter into agreements involving large payments or deals. It holds funds securely until all contract terms are fulfilled, such as the delivery of goods or the completion of services.

4) Online Payment Escrow

Online payment Escrow is commonly used in digital platforms, especially for e-commerce or freelance work. The buyer deposits money into an Escrow Account and the funds are released only after the product is delivered or the service is completed. This saves both buyers and sellers from fraud or non-payment.

5) Mergers and Acquisitions (M&A) Escrow

In mergers and acquisitions, Escrow Accounts are used to hold a portion of the purchase price for a specific period. This ensures that any post-deal obligations, such as warranties or claims, are properly addressed. It provides security to the buyer while also protecting the seller’s interests.

Digitalising Escrow

With the rise of technology, Escrow services are evolving rapidly. Digital Escrow platforms now allow users to manage transactions online with greater convenience and transparency. They offer features like:

1) Real-time Tracking of Funds:

Users can track the status of their funds in real time. This improves transparency and keeps both parties informed throughout the transaction.

2) Automated Payment Release:

Modern Escrow systems use automation to release funds once all agreed-upon conditions are met. This reduces delays and ensures timely transactions.

3) Secure Digital Documentation:

All agreements, contracts, and records are stored digitally. This makes it easier to access documents and reduces the risk of loss or damage.

4) Enhanced Security Measures:

Digital Escrow platforms use encryption and verification methods to protect sensitive information. This helps prevent fraud and ensures safe transactions.

5) Global Accessibility:

Digital Escrow allows people from different locations to complete transactions easily. It is especially useful for international deals and remote business activities.

Overall, digitalising Escrow reduces paperwork, speeds up processes and enhances security through proper security and verification systems.

Evaluate financial systems and ensure compliance with the

Audit and Assurance (AA) Course

– Sign up soon!

Example of Escrow in Home Buying

Let’s imagine that a person is buying a house. The buyer is ready to purchase a property for £300,000. As part of the agreement, the buyer deposits £10,000 into an Escrow Account managed by a trusted third party. This amount shows the buyer’s commitment to the purchase.

While the money is held safely, a few important steps take place. The property is inspected, the home loan is approved, and all legal checks are completed. During this time, the seller cannot use the money, and the buyer knows it is secure.

Once everything is completed, the Escrow agent releases the full payment to the seller and the property is officially transferred to the buyer. If any problem is found and the buyer decides not to continue (as per the agreement), the Escrow Account makes sure the deposit is returned.

Advantages of an Escrow Account

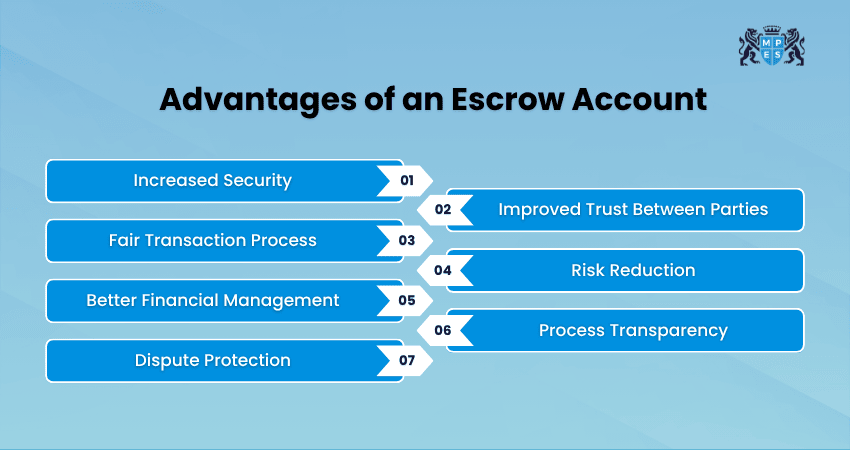

Escrow Accounts offer several advantages that make them a preferred choice for secure transactions. Some of those advantages include:

1) Increased Security:

Escrow Accounts keep your money safe by holding it with a trusted third party. This minimises the risk of fraud or misuse during a transaction.

2) Improved Trust Between Parties:

Since neither party controls the funds directly, both parties feel more confident and secure throughout the process.

3) Fair Transaction Process:

Money is only released when all agreed conditions are met. This makes the transaction fair for both the buyer and the seller.

4) Risk Reduction:

Escrow helps minimise risks such as non-payment or incomplete delivery by protecting both sides until the deal is completed.

5) Better Financial Management:

For ongoing Escrow Accounts, such as those linked to mortgages, payments like taxes and insurance are managed efficiently and on time.

6) Process Transparency:

Both parties can clearly understand when and how the funds will be released, which reduces confusion and misunderstandings.

7) Dispute Protection:

If any issue arises, the Escrow agreement provides a clear structure to handle disputes and decide what happens to the funds.

Disadvantages of an Escrow Account

While Escrow Accounts offer many benefits, they also come with a few limitations that are important to understand. Below are the advantages that you need to consider:

1) Escrow services often involve fees, which can increase the overall cost of the transaction.

2) The money is held by a third party, so neither party can use it until all conditions are met.

3) Transactions may take longer if there are delays in meeting conditions or completing paperwork.

4) For those unfamiliar with Escrow, the process can feel confusing at first.

5) Funds are only released when all terms are met, which can sometimes slow down the process if there are minor issues.

Common Misconceptions About Escrow Accounts

Escrow Accounts are often misunderstood, especially by those who are new to financial transactions. Here are some of the popular misconceptions about them:

1) Escrow is Only Used for Property Deals:

Many people think Escrow is limited to buying homes, but it is also used in business transactions, online payments, and legal agreements.

2) Escrow Guarantees a Risk-free Transaction:

While Escrow reduces risks, it does not completely eliminate them. Clear terms and proper verification are still important.

3) The Buyer or Seller Controls the Money:

In reality, a neutral third party manages the funds, ensuring fairness for both sides.

4) Escrow is Unnecessary for Small Transactions:

Even smaller deals can benefit from Escrow, especially when trust between parties is limited.

5) Funds are Released Automatically:

Money is only released when all agreed conditions are met, not simply based on time or assumptions.

6) Escrow Accounts are Complicated to Use:

Although they may seem complex at first, Escrow processes are usually structured and easy to follow once understood.

Conclusion

Escrow Accounts play a prominent role in making financial transactions safer and more trustworthy. Whether used in business deals, online payments, or long-term financial arrangements, a proper knowledge of What is an Escrow Account provides a simple yet effective way to manage financial risk. By understanding its purpose and process, you can handle important transactions with clarity.

Develop real-world financial and analytical skills with ACCA Applied Skills Training – Join now!

Frequently Asked Questions

Q. How to Manage an Escrow Account?

To manage an Escrow Account, regularly review statements, ensure sufficient funds are maintained, and track all incoming and outgoing payments. You need to be aware of due dates and agreement terms and conduct regular reconciliations to ensure funds are released strictly according to the agreed contract terms.

Q. What is the Minimum Balance for Escrow?

The minimum balance in an Escrow Account depends on the agreement terms and legal requirements. Typically, it must be sufficient to cover expected payments, taxes, fees, or obligations, ensuring funds are always available to meet agreed conditions.

Q. What is an Escrow Disbursement?

An Escrow disbursement is the release of funds from an Escrow Account to the designated party once all contractual conditions are satisfied. These conditions may include inspections, approvals or legal formalities specified in the Escrow agreement.