Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

Setting up a Limited Company in UK: A Comprehensive Guide for 2026

Set up a Limited Company in the UK by registering with Companies House and following key steps, costs, and legal requirements to start smoothly. Understand the required documents and timelines to ensure compliance and launch your business with confidence. Avoid delays and complete your company registration smoothly.Table Of Contents

44 7452 122728

44 7452 122728

04-Apr-2026

04-Apr-2026

Author-Jenny Morris

Thinking of starting your own business but unsure where to begin? You are not alone. Many people reach a point where they want more control, better credibility, and protection for their personal finances. That is exactly why learning how to Set up a Limited Company becomes an important step towards building something secure and professional.

As your idea grows from a side hustle into a serious venture, this blog explains how to Set up a Limited Company in a simple and practical way. It covers the key steps, costs, and timelines involved, helping you move forward with clarity, confidence, and a clear direction. Now, let’s get started!

What is a Limited Company?

A limited company is a business structure where the company is legally separate from its owners, meaning it can own assets, enter into contracts, and be responsible for its own debts. One of its main features is limited liability, which protects the personal assets of the owners. In the UK, limited companies must be registered with Companies House and follow legal and financial rules.

Based on how they are structured and operated, limited companies are generally classified into two main types: those limited by shares and those limited by guarantee. Companies limited by shares are typically profit-making businesses owned by shareholders, while companies limited by guarantee are usually non-profit organisations run by members rather than shareholders.

How to Set up a Limited Company: Step-by-Step Process?

Setting up a Limited Company in the UK involves registering your business as a separate legal entity, protecting your personal finances while meeting requirements set by Companies House and HM Revenue and Customs. Understanding how to Set up a Limited Company ensures a smooth and compliant start, as outlined in the steps below:

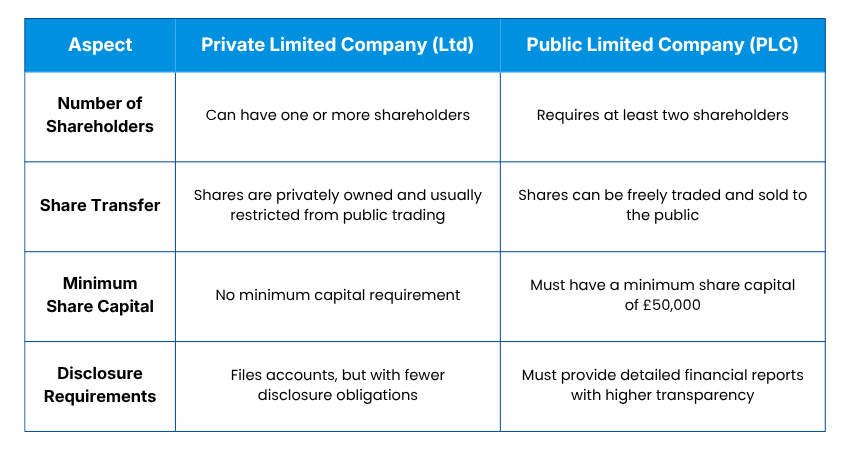

1) Choose the Type of Limited Company You Want to Form

Choosing the right type of limited company is the first step in setting up your business. In the UK, companies are commonly limited by shares for profit-making or limited by guarantee for non-profit purposes. Within this, you can form a Private Limited Company or a Public Limited Company, depending on your growth plans and funding needs.

This choice determines how profits are distributed, ownership is structured, and responsibilities are handled. Private companies are usually smaller and cannot sell shares to the public, while public companies can raise capital by offering shares openly. Selecting the right type ensures compliance and long-term stability.

2) Select a Name for Your Company

Selecting a suitable company name is an important step, as it represents your business identity and brand. The name must be distinctive, not too similar to existing companies, and should avoid restricted or sensitive terms unless proper approval is obtained from authorities to ensure full legal compliance.

A well-chosen name helps build trust and recognition among customers and stakeholders. It is also essential to check name availability before registration to avoid delays and ensure compliance with UK naming regulations during the company formation process. Choosing a clear and relevant name can also strengthen your market presence from the start.

3) Appoint at Least One Director for the Company

Every limited company must appoint at least one director who’s legally accountable for managing the business. The director ensures that the company complies with financial reporting, legal obligations, and submits required documents on time to relevant authorities to maintain compliance and avoid penalties.

They play a key role in decision-making and maintaining compliance with Companies House. Choosing a responsible and capable director helps ensure proper governance and supports the company’s long-term growth and stability. A strong director also contributes to building trust with stakeholders and regulators.

4) Decide Who the Shareholders of the Company Will be

Shareholders are the owners of the company and hold shares that represent their ownership stake. They may receive profits in the form of dividends and can influence important business decisions based on their shareholding percentage and level of voting rights within the company structure overall.

A company can have one or multiple shareholders depending on its structure. Clearly defining ownership, roles, and responsibilities from the start helps avoid conflicts and ensures smoother decision-making as the business grows and evolves over time. Proper planning also supports transparency and long-term business success.

5) Understand the Records You are Required to Maintain as a Limited Company in the UK

Maintaining accurate and up-to-date records is a legal requirement for all limited companies in the UK. These include financial accounts, details of directors and shareholders, as well as key legal documents like the Memorandum of Association and Articles of Association, which define how the company is formed and governed.

Companies must also submit annual accounts and confirmation statements to HM Revenue and Customs and Companies House. Proper record-keeping ensures compliance, improves transparency, and helps avoid penalties while supporting effective and organised Business Management.

Develop practical audit skills and excel in assurance engagements with the Assurance (AS) Training – Join today!

When to Set up a Limited Company?

The right time to Set up a Limited Company depends on your business growth, income, and goals. Timing can also affect your accounting deadlines and tax planning. The points below explain these factors:

1) How Does Your Company Formation Date Affect Accounting Deadlines?

Your company’s formation date determines your accounting period and filing deadlines. Once registered with Companies House, you must submit accounts and tax returns within set time limits.

For example, Corporation Tax is usually due nine months and one day after your accounting period ends, while your Company Tax Return must be filed within twelve months. Choosing the right formation date can give you more time to organise your records and meet deadlines.

2) Does the Month You Form a Company Impact How Much Tax You Pay?

The month you form your company does not change the total tax you pay, but it affects when payments are due. Your incorporation date sets your financial year-end, which influences tax deadlines and overall financial planning.

Choosing the right month can help you align your financial year with your business cycle. This makes it easier to control cash flow, prepare for tax payments, and maintain better control over your company’s finances throughout the year.

3) When Should You Switch from a Sole Trader to a Limited Company?

You should consider switching when your profits grow and a limited company becomes more tax-efficient. It is also a good option if you want to protect your personal assets and separate your business from your personal finances.

Switching at the right time can improve your business credibility and support long-term growth. It also allows you to take advantage of financial benefits while ensuring your business remains compliant with legal and regulatory requirements.

Develop practical skills in costing, forecasting and business decision-making through the

Management Information (MI) Training

– Join now!

What is the Cost to Set up a Limited Company in 2026?

The cost of setting up a limited company in the UK has increased from 1 February 2026, with the standard online registration fee now £100 through Companies House. If you require faster processing, same-day incorporation costs £156, while registering by post is priced at £124.

Beyond the initial setup, businesses should also consider ongoing expenses, such as the £50 annual confirmation statement fee. Overall, while the minimum cost starts at £100, the total expense may vary depending on the registration method and any additional services you choose.

How Long Does it Take to Set up a Limited Company?

Setting up a limited company in the UK is generally a quick process, with online applications often completed within 24 to 48 hours. However, the total time can vary depending on preparation, accuracy, and external factors that influence how smoothly your application is processed, as explained in the key factors below:

1) Company Name Availability

The availability of your company name can impact how quickly you complete registration. If your preferred name is already taken or too similar to an existing business, you will need to choose another.

a) Check name availability in advance

b) Avoid restricted or sensitive words

c) Keep alternative name options ready

This helps prevent delays during the application process.

2) Accuracy of Your Details

Providing accurate and complete information is one of the most important factors for quick approval. Even small mistakes can lead to delays or rejection, making it essential to review everything carefully before submission.

a) Double-check director and shareholder details

b) Ensure the correct registered address

c) Verify spelling and legal information

Careful review before submission can significantly speed up the process.

Understand tax systems, compliance and calculations with confidence and clarity with the

Principles of Taxation (PTX) Training

– Register today!

3) Application Method

The method you choose for registration has a direct impact on how quickly your company is set up. Some options are much faster than others, so selecting the right one can save valuable time.

a) Online Application: Usually processed within 24 hours

b) Same-day Service: Completed within hours (if submitted early)

c) Postal Application: Can take 8 to 10 working days

Choosing the right method can save considerable time.

4) Time of Registration

The timing of your application plays a massive role in processing speed. Submitting your application at the right time can help avoid unnecessary delays.

a) Applications submitted early in the day are processed faster

b) Weekend or late submissions may be delayed

c) Public holidays can extend processing times

Planning your submission time helps avoid unnecessary waiting.

5) Companies House Workload

The processing times can change based on how busy Companies House is at the time of your application. External factors like workload can influence how quickly approvals are completed.

a) Busy periods can slow down approvals

b) High volumes of applications may cause slight delays

c) Peak filing seasons can extend processing time

Understanding these factors helps set realistic expectations.

Conclusion

Setting up a limited company in the UK can be quick and hassle-free when you plan ahead and avoid common errors. By understanding key factors that affect timelines, you can Set up a Limited Company efficiently, ensuring smooth registration, full compliance, and a strong start for your business journey.

Build strong foundations in accounting, finance, and business for success through the ACA Certificate Level Training – Join now!

Frequently Asked Questions

Q. Can I Start a Ltd Company on my Own?

Yes, you can start and run a Limited Company (Ltd) on your own. As the sole owner, you act as both director and shareholder, managing all responsibilities while the company remains a separate legal entity, protecting your personal assets from business liabilities.

Q. Is Ltd Better Than a Sole Trader?

A Limited Company (Ltd) is better for high-profit or higher-risk businesses as it offers limited liability and tax benefits. A sole Trader is ideal for small, low-risk businesses because of its simplicity and lower administrative burden. The best choice depends on your income, risk level, and growth plans.

Q. Can One Person Run a Ltd Company?

Yes, one person can run a Limited Company (Ltd). In the UK, a single individual can act as both the sole director and shareholder, managing the business independently. The company remains a separate legal entity, offering limited liability and protecting personal assets.