Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

What Are Management Accounts? Components, Purpose, and Examples

Management Accounts are internal financial reports that provide insights into a company’s performance to support planning, decision-making, and cost control. They help managers track performance, manage cash flow, and identify issues early. With timely data, businesses can make better decisions and improve efficiency.Table Of Contents

44 7452 122728

44 7452 122728

23-Apr-2026

23-Apr-2026

Author-Gary Moore

Running a business is not just about generating revenue; it is about clearly understanding your financial performance at every stage. This is where Management Accounts play a key role, helping organisations track expenses, monitor profits, and improve the efficiency of their business operations and services.

To build on this, it is important to understand What are Management Accounts and how they support better decision-making. In this blog, you will explore their key components, benefits, and practical examples, helping you use financial insights effectively to improve performance and plan for growth. Read on to learn more!

What are Management Accounts?

Management Accounts are internal financial reports prepared regularly, usually monthly or quarterly, to give business owners and managers a clear view of performance. They provide detailed and timely information that helps track income, expenses, and overall business activities, including how efficiently products and services are delivered.

Unlike statutory accounts, which are created annually for legal and external purposes, Management Accounts are not required by law. However, they are essential for monitoring cash flow, analysing profitability, and supporting informed, strategic decision-making within the organisation.

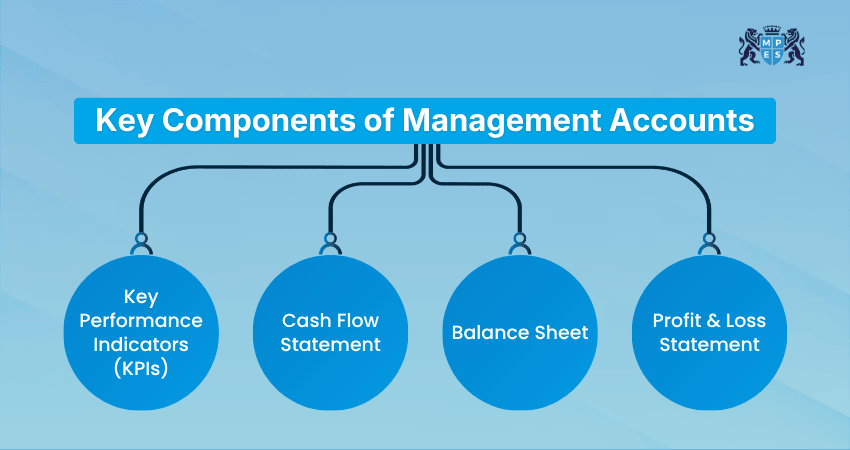

Key Components of Management Accounts

Management Accounts include key financial and performance elements that give a clear view of a company’s operations and financial position. These help managers assess efficiency, profitability, and overall performance. The main components are:

1) Key Performance Indicators (KPIs)

KPIs are measurable values that indicate how effectively a business is achieving its objectives. These indicators vary depending on the organisation’s goals and may include revenue growth, profit margins, or customer acquisition rates.

They help managers focus on key areas that drive success. By tracking KPIs regularly, organisations can quickly identify performance gaps and take corrective measures to improve outcomes and ensure consistent progress toward strategic targets.

2) Cash Flow Statement

A cash flow statement indicates how money moves in and out of a business over a specific period. It highlights operating, investing, and financing activities, giving managers a clear view of liquidity and financial stability.

This component helps organisations manage their cash effectively and avoid shortages. By analysing cash flow, businesses can ensure they have enough funds to meet liabilities, invest in growth, and maintain smooth daily operations.

3) Balance Sheet

The balance sheet gives an overview of a company’s financial position at a certain point in time. It includes assets, liabilities, and equity, helping managers understand what the business owns and owes.

This information is essential for evaluating financial stability and risk. Managers use balance sheets to assess whether the organisation has a strong financial foundation and to make decisions about investments, funding, and resource allocation.

4) Profit & Loss Statement

The profit and loss statement, also known as the income statement, shows a company’s revenues and expenses over a period. It helps determine whether the business is making a profit or incurring losses.

This report is vital for analysing financial performance. It allows managers to identify cost patterns, evaluate profitability, and implement strategies to improve margins and overall business efficiency.

Purpose of Preparing Management Accounts

Management Accounts are prepared to support better decision-making and business planning. They provide clear insights into financial and operational performance, helping organisations respond quickly to changes. The key purposes are outlined below:

1) Better Financial Visibility

Management Accounts offer a clear and detailed view of financial performance. They provide regular updates on income, expenses, and profitability, allowing managers to understand how the business is performing at any given time.

This visibility helps identify trends and patterns that may not be obvious in annual reports. As a result, businesses can take proactive measures to address issues and improve financial outcomes effectively.

2) Better and Accurate Decision-making

Accurate financial data is important for making informed decisions. Management Accounts provide reliable information that helps managers evaluate options, assess risks, and choose the best course of action for the organisation.

With access to timely insights, decision-making becomes more strategic and less reactive. This improves overall efficiency and ensures that business actions are aligned with organisational goals and long-term plans.

3) Better Cash Flow Management

Effective cash flow management is essential for business sustainability. Management Accounts help track cash inflows and outflows, enabling organisations to maintain adequate liquidity and avoid financial difficulties.

By understanding cash patterns, businesses can plan payments, manage expenses, and allocate resources efficiently. This ensures smooth operations and reduces the risk of cash shortages or financial disruptions.

4) Fast Issue Detection

Management Accounts allow businesses to identify problems quickly. Regular reporting highlights deviations from expected performance, making it easier to detect issues such as rising costs or declining revenue early.

Early detection enables timely corrective action. This helps organisations minimise risks, improve efficiency, and maintain stability in a competitive business environment where quick responses are essential.

Build strong skills in cost management and financial planning through the

Managing Costs and Finance (MA2) Training

– Join soon!

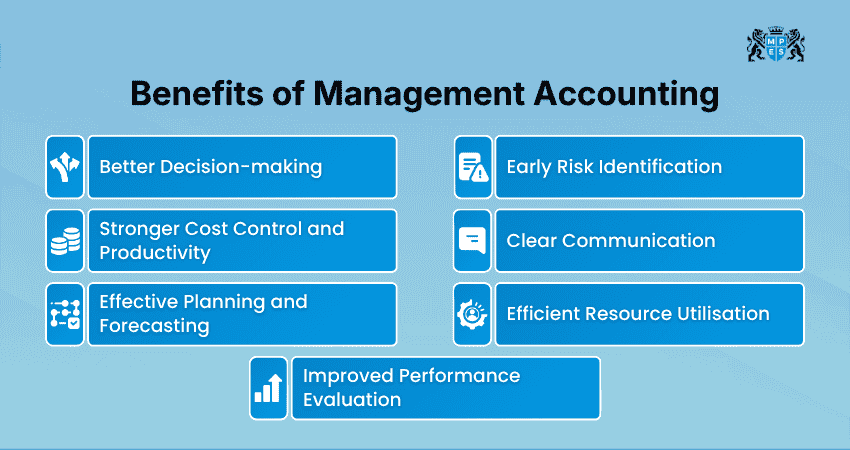

Benefits of Management Accounting

Management Accounting delivers measurable value by improving control, efficiency, and overall business performance. It helps organisations use financial data effectively to achieve their goals. Key benefits include:

1) Better Decision-making: Delivers accurate, real-time data that helps managers make informed choices about pricing, investments, and business operations.

2) Stronger Cost Control and Productivity: Highlights inefficiencies and unnecessary expenses, allowing businesses to reduce costs without affecting quality.

3) Effective Planning and Forecasting: Uses past data and market trends to support budgeting, forecasting, and long-term strategies.

4) Improved Performance Evaluation: Helps set clear targets and measure the performance of teams and departments effectively.

5) Early Risk Identification: Detects potential risks in advance and supports strategies to reduce financial and operational uncertainties.

6) Clear Communication: Encourages transparent, data-based communication about financial goals and performance across the organisation.

7) Efficient Resource Utilisation:

Ensures that financial and operational resources are used in the most effective way to achieve business objectives.

Drawbacks of Management Accounting

While Management Accounting offers many benefits, it also has some limitations that businesses should consider. These drawbacks can affect how effectively the information is used in decision-making:

1) Reliance on Historical Data: Uses past data, which may not always reflect current or future business conditions.

2) Lack of Standardisation: Does not follow fixed rules, leading to variations in reporting and interpretation.

3) High Implementation Cost: Requires time, tools, and expertise, making it costly for some organisations.

4) Provides Data, Not Decisions: Supports decision-making but does not offer final solutions.

5) Subject to Bias:

Internal preparation can lead to personal judgement influencing the reports.

Who Uses Management Accounts?

Management Accounts are used by various stakeholders to understand a business’s financial performance and support informed decision-making. These reports provide valuable insights that help both internal and external users assess financial health and plan effectively:

1) Owners and Managers: Use Management Accounts to monitor performance, control costs, and make strategic business decisions.

2) Investors: Review these reports to evaluate profitability, growth potential, and the overall financial stability of the business.

3) Banks and Lenders: Analyse Management Accounts to assess creditworthiness and decide whether to approve loans or financing.

4) Factoring and Invoice Discounting Providers: Use them to evaluate cash flow and determine funding against outstanding invoices.

5) Accountants: Prepare and interpret Management Accounts to provide financial insights and support business planning.

6) Tax Planners: Use the data to plan tax strategies efficiently and ensure compliance while optimising tax liabilities.

Develop practical Management Accounting skills for business success with the

Management Accounting (FMA) Training

– Register now!

Example of Management Accounts

A clear example of Management Accounts can be seen in a monthly report prepared by a company such as ABC Retail Ltd to track its financial performance. This Management Accounts example includes revenue, expenses, profit, cash flow, and key performance indicators, including service performance metrics.

For March, ABC Retail Ltd reported total sales of £50,000, with the cost of goods sold at £20,000 and operating expenses of £15,000, including rent, salaries, and utilities. This resulted in a net profit of £15,000 for the month.

In terms of cash flow, the company received £45,000 from customers and paid £30,000 to suppliers and staff, maintaining a positive cash balance. Key performance indicators showed a 10% increase in sales and a 30% profit margin, helping managers make informed decisions and plan growth strategies.

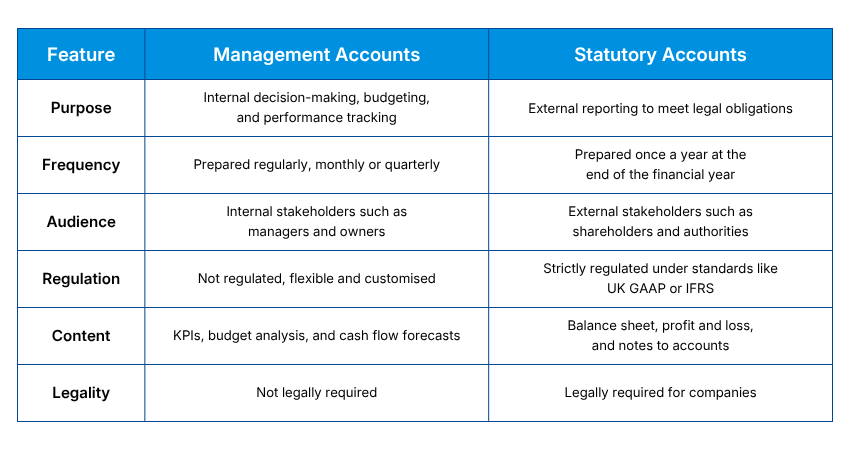

Difference Between Management Accounts and Statutory Accounts

Management Accounts and statutory accounts differ mainly in their purpose and use. Management Accounts are prepared for internal decision-making, helping managers plan, control costs, and track performance regularly.

Statutory Accounts, on the other hand, are prepared to meet legal requirements and are shared with external stakeholders. They follow standard formats and provide a formal summary of a company’s financial position at the end of the financial year.

Conclusion

In essence, understanding What are Management Accounts is essential for businesses aiming to improve financial control and decision-making. These reports help monitor performance, manage costs, and support strategic planning. By using Management Accounts regularly, organisations can respond quickly to changes, improve efficiency, and ensure long-term financial stability and growth.

Start your accounting career with essential bookkeeping and financial management skills with the ACCA Foundations Training – Join now!

Frequently Asked Questions

Q. Is a P&L the Same as Management Accounts?

No, a P&L is not the same as Management Accounts. A Profit and Loss statement shows only revenues and expenses over a period. Management Accounts are broader internal reports that include the P&L, balance sheet, cash flow forecasts, and key metrics to support informed decision-making.

Q. What are the Four Types of Financial Statements?

The four key financial statements are the balance sheet, profit and loss statement, cash flow statement, and statement of changes in equity. These provide a complete view of a company’s financial performance and position.

Q. What are the Five Functions of Management Accounting?

The five key functions include planning, controlling, decision-making, forecasting, and performance evaluation. These functions help organisations manage resources effectively and achieve their business objectives through structured financial analysis.