Have Any Question?

Have Any Question?

+44 7452 122728

+44 7452 122728

Back

Back

Financial Planning: What It Is and How to Create a Financial Plan

Financial Planning is the process of managing money, setting clear financial goals, and creating strategies to achieve long-term financial stability. It helps control spending, reduce debt and prepare for the future. It also encourages better saving habits, smarter investment decisions and builds confidence in managing your finances.Table Of Contents

44 7452 122728

44 7452 122728

09-May-2026

09-May-2026

Author-Maria Thompson

Imagine reaching the end of the month with no stress about bills or savings. No worrying about upcoming expenses, no last-minute adjustments and no confusion about where your money went. Instead, you feel organised, prepared and in full control of your finances. For many people, this feels out of reach. But that’s where Financial Planning makes a difference.

It helps you understand your finances, set realistic goals and create a clear path towards achieving them. In this blog, we will explore What is Financial Planning, why it matters and how to build a plan that supports your financial success. Let's get started!

What is Financial Planning?

Financial Planning is the process of organising your finances to meet your short-term and long-term goals. It involves assessing your income, expenses, savings, investments and risks, and then building a strategy that aligns with your lifestyle and future goals.

At its core, Financial Planning is not just about money. It is about making informed decisions. It helps you understand where your money goes, how much you can save and how you can grow your wealth over time. From buying a home to retiring comfortably, every major life milestone benefits from a structured financial approach.

Why Do One Need a Financial Plan?

Without a proper Financial Plan, it is easy to lose track of your money. You may be put into a situation where it is easy to overspend, save less, or miss out on important financial goals.

Thus, a Financial Plan helps you:

1) Set realistic and achievable goals

2) Control unnecessary spending

3) Build savings and emergency funds

4) Reduce debt efficiently

5) Prepare for future uncertainties

More importantly, it gives you clarity. Instead of guessing whether you are doing “okay financially,” you have measurable benchmarks to track your progress.

How to Create Financial Planning?

Creating a Financial Plan may seem complex at first, but it becomes much easier when broken down into clear and manageable steps. A structured approach helps you gain control over your finances, reduce risks, and work towards long-term financial security. Let’s explore the process step by step:

1) Decide Between Self-planning or Hiring a Financial Advisor

The first step is choosing how you want to approach your financial planning. Some individuals prefer managing their finances independently using budgeting tools and apps. Alternatively, you can seek professional guidance from a Financial Advisor who can assist with investment strategies, tax planning, and long-term wealth management based on your financial goals.

2) Establish an Emergency Fund

An emergency fund acts as a financial safety net. It covers unexpected expenses such as medical emergencies, job loss, or urgent repairs. Ideally, you should aim to save at least three to six months’ worth of living expenses. This fund should remain easily accessible, typically in a savings account rather than long-term investments.

3) Develop a Strategy to Reduce Debt and Control Expenses

Debt can quickly become a barrier to financial growth if not managed properly. Start by listing all your debts, including interest rates and repayment schedules. You need to focus on paying off high-interest debts first, avoiding unnecessary borrowing and creating a monthly budget to track expenses.

4) Identify and Manage Financial Risks

Financial risks can come at any time. These may include unexpected health issues, business losses or market fluctuations. Having insurance helps protect you from these risks. Health insurance, life insurance and property insurance are some common examples. Being prepared in advance helps reduce financial stress and keeps your long-term plans on track.

5) Start Investing Based on Your Goals

Once you have control over your savings and expenses, the next step is to start investing. Investing helps your money grow over time and supports your long-term financial goals. Instead of keeping all your money in savings, putting it into the right investments can generate better returns. Spreading your investments across different areas also reduces risk.

6) Incorporate Tax Planning into Your Strategy

Taxes can significantly impact your income and investments. Effective tax planning ensures you maximise your earnings while staying compliant with regulations. You can reduce your tax burden by using tax-saving investment options, claiming available deductions, and planning your income wisely. Even small tax efficiencies can lead to big savings over time.

7) Plan for Estate and Wealth Transfer

Estate planning is about deciding how your assets will be managed and passed on in the future. It ensures that your money, property and investments are distributed according to your wishes and that your family is financially protected. This can include writing a will, naming beneficiaries and organising your assets properly.

8) Regularly Review and Update Your Financial Plan

A Financial Plan is not like you create it once and forget. Your income, expenses and life situations will change over time, so your plan should be updated. Regular reviews help you stay on track and ensure your financial strategy remains effective. You need to review your plan at least once a year or after major events such as a job change, marriage, or a significant financial gain or loss.

Learn how to analyse financial data and support business growth with the Financial Management (FM) Course – Register today!

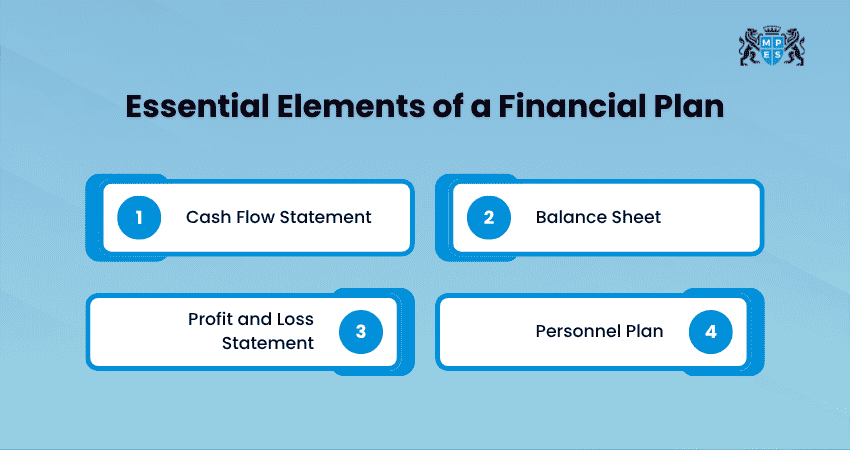

What Must an Ideal Financial Planning Include?

An effective Financial Plan should include key financial statements and structured insights that provide a complete picture of your financial position. Here are the things you need for your Financial Planning:

1) Cash Flow Statement

A cash flow statement shows how money moves in and out of your finances over a specific period. It helps you understand how much you earn, spend and save each month. This statement is useful for identifying areas where you can cut costs and improve savings.

2) Balance Sheet

A balance sheet provides a snapshot of your financial position at a given time. It lists your assets, such as savings and property, and your liabilities, such as loans and debts. By comparing these, you can calculate your net worth and track your financial progress over time.

3) Profit and Loss Statement

A profit and loss statement is mainly used for businesses. It shows the total income, expenses, and profit over a period. This helps in understanding how well a business is performing and where changes are needed to improve profitability.

4) Personnel Plan

A personnel plan outlines the people required to manage operations and the costs associated with them. It includes salaries, benefits and staffing needs. This is especially important for businesses, as employee costs often make up a large part of total expenses.

What is Corporate Financial Planning and Analysis?

Corporate Financial Planning and Analysis (FP&A) refers to the process organisations use to manage budgeting, forecasting and financial decision-making. It involves analysing financial data to support strategic planning and improve business performance. Usually this team focus on:

1) Budget preparation

2) Financial forecasting

3) Performance analysis

4) Risk assessment

This process ensures that a company’s financial strategy aligns with its business goals. It also helps leadership make data-driven decisions, reduce uncertainty and improve efficiency.

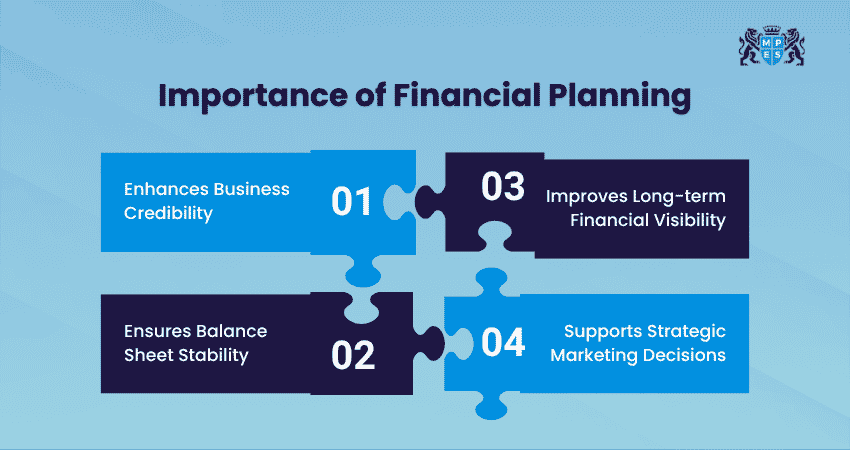

Why Financial Planning is Important for Your Business?

Financial Planning is essential for businesses as it helps manage money effectively, prepare for uncertainties, and support informed decision-making. A well-structured financial plan not only improves stability but also enables sustainable growth and long-term success. Here are the key reasons why it is important for businesses:

1) Enhances Business Credibility

A well-prepared Financial Plan builds trust among investors, lenders and stakeholders. It shows that your business is organised, financially aware and capable of managing its resources responsibly. This credibility makes it easier to secure funding, attract partnerships and grow your business.

2) Ensures Balance Sheet Stability

Financial Planning helps maintain a healthy balance between assets and liabilities. It ensures that your business does not take on excessive debt and that resources are used efficiently. A stable balance sheet reflects strong financial health and reduces the risk of financial problems.

3) Improves Long-term Financial Visibility

A Financial Plan gives you a clear view of your business’s future. It helps you forecast income, expenses, and potential risks, allowing you to prepare in advance. This long-term visibility makes it easier to set realistic goals and make strategic decisions.

4) Supports Strategic Marketing Decisions

Marketing requires proper budgeting and planning. Financial Planning ensures that you allocate the right amount of money to marketing activities. It helps you invest in strategies that deliver results while avoiding unnecessary spending, leading to better returns on investment.

Gain practical insights into tax systems and business planning with the Business Planning Tax (BPT) Course – Sign up soon!

Benefits of Making a Financial Plan

Having a Financial Plan brings structure and clarity to how you manage your money. Whether for personal use or business, it can make a significant difference in your financial growth. Here are the benefits of it:

1) Helps you track your income and expenses, making it easier to control spending

2) Gives you a clear direction for saving, investing and achieving future plans

3) Encourages regular saving and builds financial discipline over time

4) Supports planning for timely repayment and reducing financial burden

5) Ensures you have a safety net for unexpected expenses

When to Update Your Financial Plan?

Updating your Financial Plan is just as important as creating it. Certain situations require immediate review, including:

1) Major life events such as marriage, childbirth, job switch or relocation

2) Significant changes in income or expenses

3) Economic shifts or market changes

4) Achieving or revising financial goals

Even without major changes, an annual review ensures that your plan remains aligned with your current needs.

Conclusion

Financial Planning is about creating a secure path for your future. The key is to start simple and stay consistent. By understanding What is Financial Planning and reviewing your finances regularly, you can build strong planning habits over time. Whether you are planning your personal finances or running a business, this helps you make better decisions, stay prepared for uncertainties and move closer to your goals with confidence.

Prepare for complex real-world financial challenges with ACA Professional Level Training – Join now!

Frequently Asked Questions

Q. How to Make a Good Financial Plan?

A good Financial Plan starts with understanding your income, expenses and goals. Create a budget, build an emergency fund, reduce debt and invest based on your risk tolerance. Regularly review your plan and adjust it as your financial situation changes.

Q. What is the 50 30 20 Rule in Financial Planning?

The 50-30-20 rule in Financial Planning is a simple budgeting method:

1) 50% of income goes to essential expenses

2) 30% is allocated for lifestyle and personal spending

3) 20% is saved or invested

This approach helps maintain a balance between spending and savings.

Q. What is Financial Planning in Management?

Financial Planning in management involves forecasting financial needs, allocating resources, and ensuring that organisational goals are achieved efficiently. It supports decision-making, risk management, and long-term business sustainability.